The SaaS VC Report 2026

The Definitive Guide to Software Venture Capital

$512B invested globally · AI dominance · Top VC rankings · Q1 2026 record quarter

Executive Summary

Welcome to the SaaS VC Report 2026, SaasRise's annual deep dive into the state of venture capital for software and SaaS companies worldwide. This report covers full-year 2025 data with Q1 2026 updates, analyzing investment trends, valuations, top VC firms, geographic distribution, and what it all means for founders and investors.

2025 was a year of extremes. Global venture capital hit $512 billion in deal value — the second-highest annual total ever — driven almost entirely by artificial intelligence. AI companies captured more than half of all VC deal value globally, reshaping the venture landscape in ways not seen since the dot-com era. Meanwhile, Q1 2026 shattered all records with $297 billion in a single quarter, fueled by unprecedented mega-rounds from OpenAI, Anthropic, xAI, and Waymo.

If you like data-driven SaaS content like this and want more, apply to join the SaasRise mastermind community.

Key SaaS Venture Capital Stats for 2025

Here are the key statistics for the software venture capital market in 2025:

- Total global VC investment was $512 billion, up 48% from $345 billion in 2024

- Total software VC investment was an estimated $200 billion, up 60% from $125 billion in 2024

- AI/ML deals captured 65.6% of all US VC deal value ($222B of $339B) and 52.7% globally

- The median Series A investment was $13.5M on a $47.0M pre-money valuation

- The median Series B investment was $32.0M on a $185.0M pre-money valuation

- The median Series C investment was $42.0M on a $255.0M pre-money valuation

- The median revenue multiple for all software venture rounds was 10.8x, up from 10.1x in 2024

- There were an estimated 9,200 software venture deals — up 12% from 8,188 in 2024

- The average software VC deal size grew to $21.7M — up 42% from $15.3M in 2024

- Global VC exit value surged to $549.2 billion — the strongest exit year since 2021

- Q1 2026 shattered all records with $297 billion in global VC funding — led by OpenAI's $122B, Anthropic's $30B, xAI's $20B, and Waymo's $16B

- Public SaaS multiples declined, with the SEG SaaS Index falling from 6.3x to 4.8x EV/Revenue

Top 20 SaaS VC Firms — Investments, Exits & AUM

The top 20 SaaS VC firms ranked by software investment count, software exits, and assets under management:

| Rank | Firm | Software Investments | Software Exits | AUM (Millions) |

|---|---|---|---|---|

| 1 | Sequoia Capital | 2,010 | 535 | $90,000 |

| 2 | Andreessen Horowitz | 1,780 | 355 | $45,000 |

| 3 | Accel | 2,050 | 540 | — |

| 4 | New Enterprise Associates | 1,420 | 520 | $27,500 |

| 5 | General Catalyst | 1,185 | 285 | $35,000 |

| 6 | Lightspeed Venture Partners | 1,210 | 340 | $26,500 |

| 7 | Tiger Global Management | 1,090 | 215 | $58,000 |

| 8 | Bessemer Venture Partners | 1,240 | 385 | $19,500 |

| 9 | Kleiner Perkins | 1,115 | 400 | $21,000 |

| 10 | Index Ventures | 1,030 | 290 | $4,500 |

The 2026 SaaS VC Power Rankings — Top 25

Combining software investment count (33%), AUM (33%), and software exits (33%), the top 25 Power Rankings are:

| # | Firm | City | Investments | Exits | AUM ($M) |

|---|---|---|---|---|---|

| 1 | Sequoia Capital | Menlo Park | 2,010 | 535 | 90,000 |

| 2 | Andreessen Horowitz | Menlo Park | 1,780 | 355 | 45,000 |

| 3 | New Enterprise Associates | Menlo Park | 1,420 | 520 | 27,500 |

| 4 | Tiger Global Management | New York | 1,090 | 215 | 58,000 |

| 5 | General Catalyst | San Francisco | 1,185 | 285 | 35,000 |

| 6 | Lightspeed Venture Partners | Menlo Park | 1,210 | 340 | 26,500 |

| 7 | Kleiner Perkins | Menlo Park | 1,115 | 400 | 21,000 |

| 8 | Bessemer Venture Partners | Redwood City | 1,240 | 385 | 19,500 |

| 9 | HongShan Capital Group | Beijing | 920 | 140 | 57,000 |

| 10 | IDG Capital | Beijing | 850 | 230 | 24,500 |

| 11 | Norwest Venture Partners | Menlo Park | 780 | 248 | 16,500 |

| 12 | Khosla Ventures | Menlo Park | 740 | 210 | 16,000 |

| 13 | Founders Fund | San Francisco | 695 | 200 | 13,000 |

| 14 | TCV | Menlo Park | 390 | 185 | 22,500 |

| 15 | Thrive Capital | New York | 425 | 95 | 18,000 |

| 16 | Bain Capital Ventures | San Francisco | 660 | 185 | 11,500 |

| 17 | Index Ventures | San Francisco | 1,030 | 290 | 4,500 |

| 18 | Redpoint Ventures | Woodside | 620 | 215 | 8,000 |

| 19 | First Round Capital | San Francisco | 810 | 270 | 3,500 |

| 20 | Entrepreneur First | London | 650 | 170 | 4,200 |

| 21 | IVP | Menlo Park | 405 | 185 | 9,200 |

| 22 | Canaan Partners | San Francisco | 490 | 175 | 7,200 |

| 23 | Sapphire Ventures | Austin | 420 | 148 | 11,000 |

| 24 | Peak XV Partners | Bengaluru | 700 | 95 | 9,500 |

| 25 | Shenzhen Capital Group | Shenzhen | 340 | 65 | 68,000 |

These 25 firms control approximately $645 billion in AUM with over $130B in dry powder. 18 of the top 25 are based in the San Francisco Bay Area.

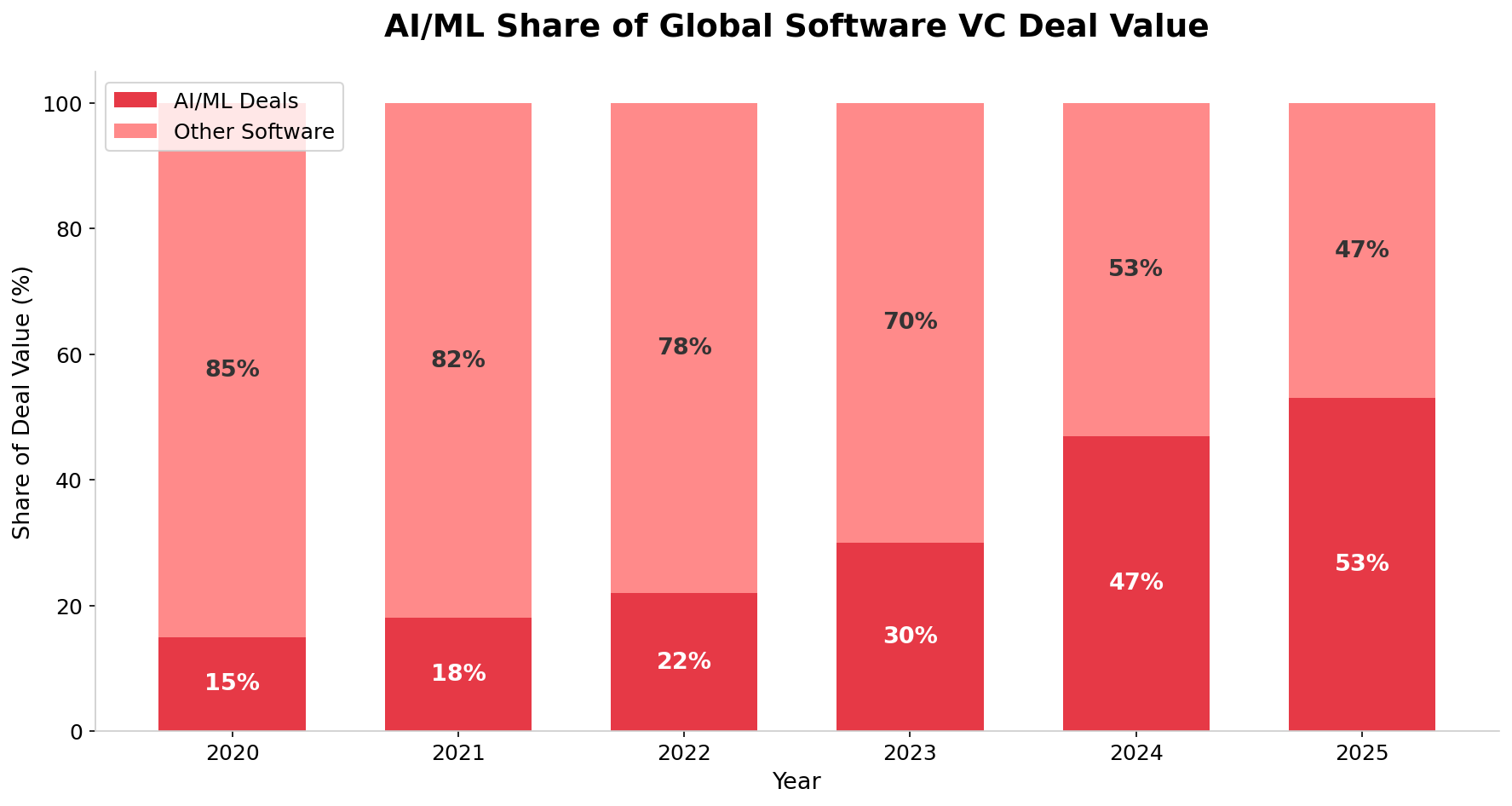

The AI Dominance of Venture Capital

The defining story of 2025 wasn't just how much money was invested — it was where it went. Artificial intelligence has fundamentally reshaped the venture capital landscape, absorbing more than half of all global deal value for the first time in history.

52.7% of all global VC deal value in 2025 went to AI/ML companies — up from 30% in 2023 and just 10% in 2015. In the US alone, AI captured 65.6% of all VC deal value ($222B of $339B).

AI/ML Share of Global Software VC Deal Value

Since the launch of ChatGPT in late 2022, AI investment has grown from $73 billion in 2022 to $222 billion in 2025 in the US alone — a 204% increase in just three years.

🤖 Largest AI Funding Rounds of 2025:

1. OpenAI — $40B (Valuation: $300B)

2. Meta/Scale AI — $14.3B (49% stake)

3. Anthropic — $13B (Valuation: $183B)

4. xAI — $10B (Elon Musk's Grok AI)

5. Databricks — $4B+ (Valuation: $134B)

6. Cursor — $2.3B (Valuation: $29.3B)

7. Anduril — $2.5B (Defense AI)

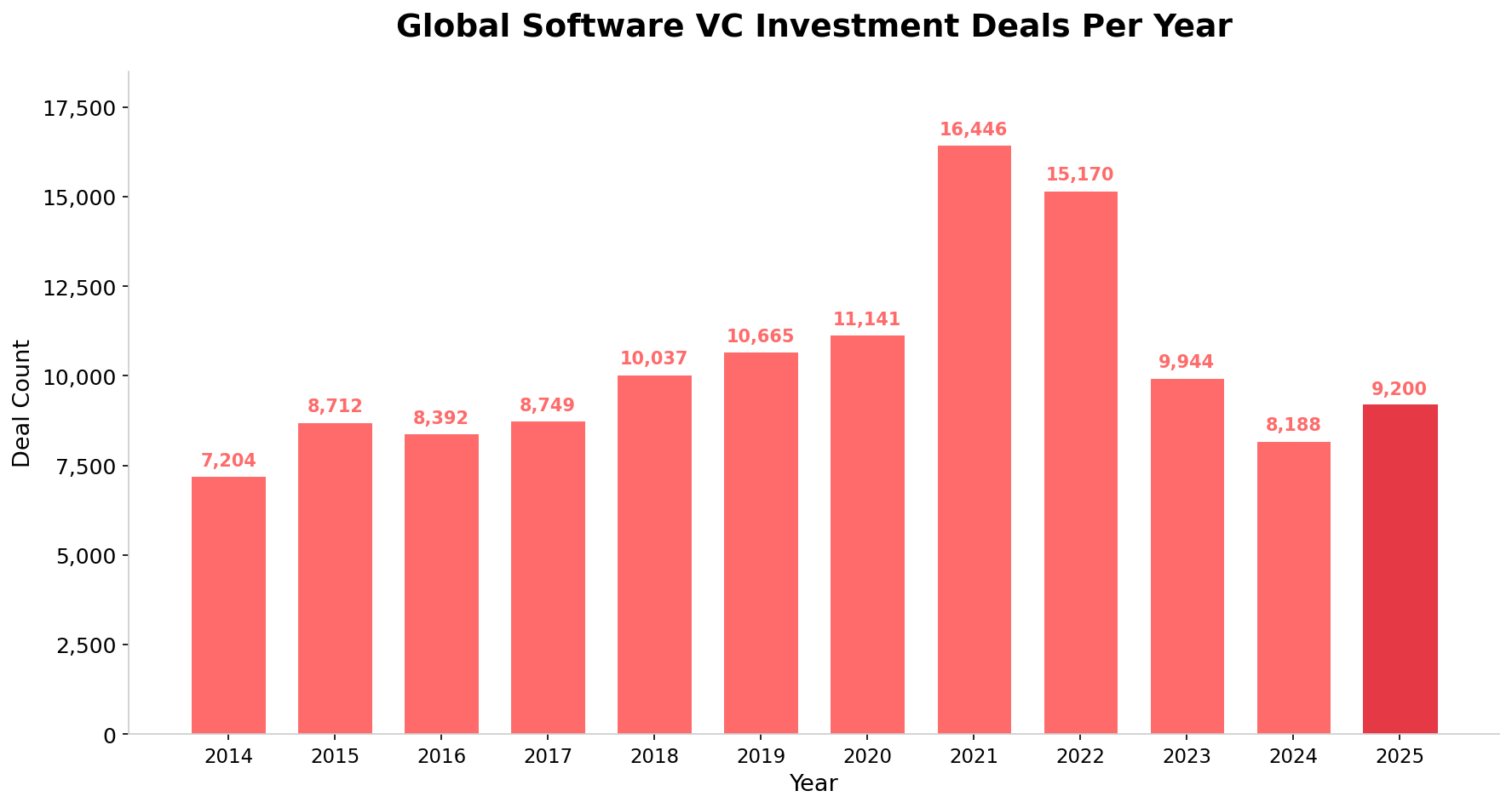

SaaS VC Deals By Year

After declining from pandemic-era peaks, software VC deal count recovered in 2025, rising approximately 12% to an estimated 9,200 deals from 8,188 in 2024. This marks the first year-over-year increase since 2021.

SaaS VC Deals By Year

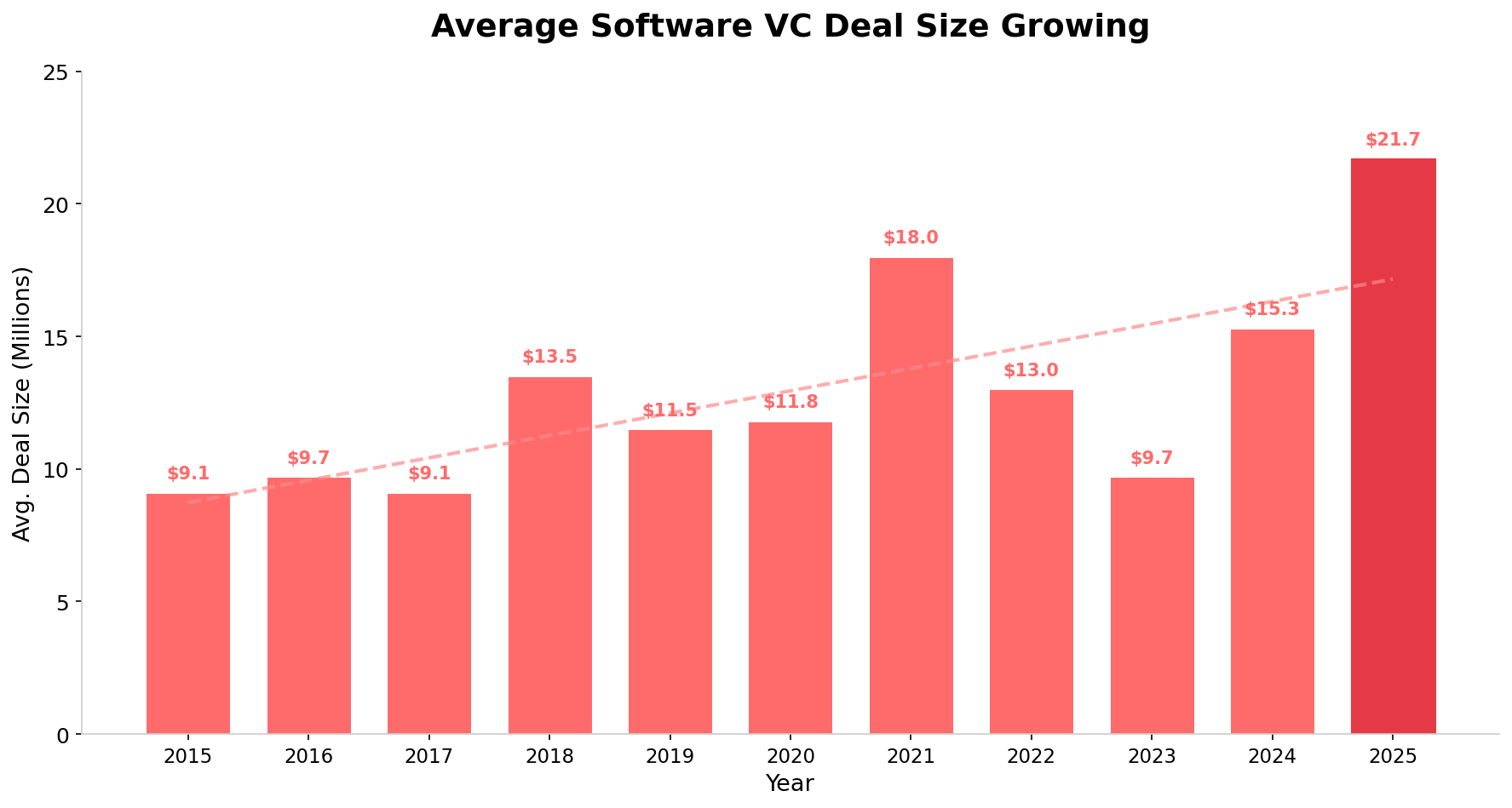

The average deal size surged to an estimated $21.7 million, up 42% from $15.3 million in 2024 — continuing the trend of fewer deals but much larger check sizes.

Average Software VC Deal Size By Year

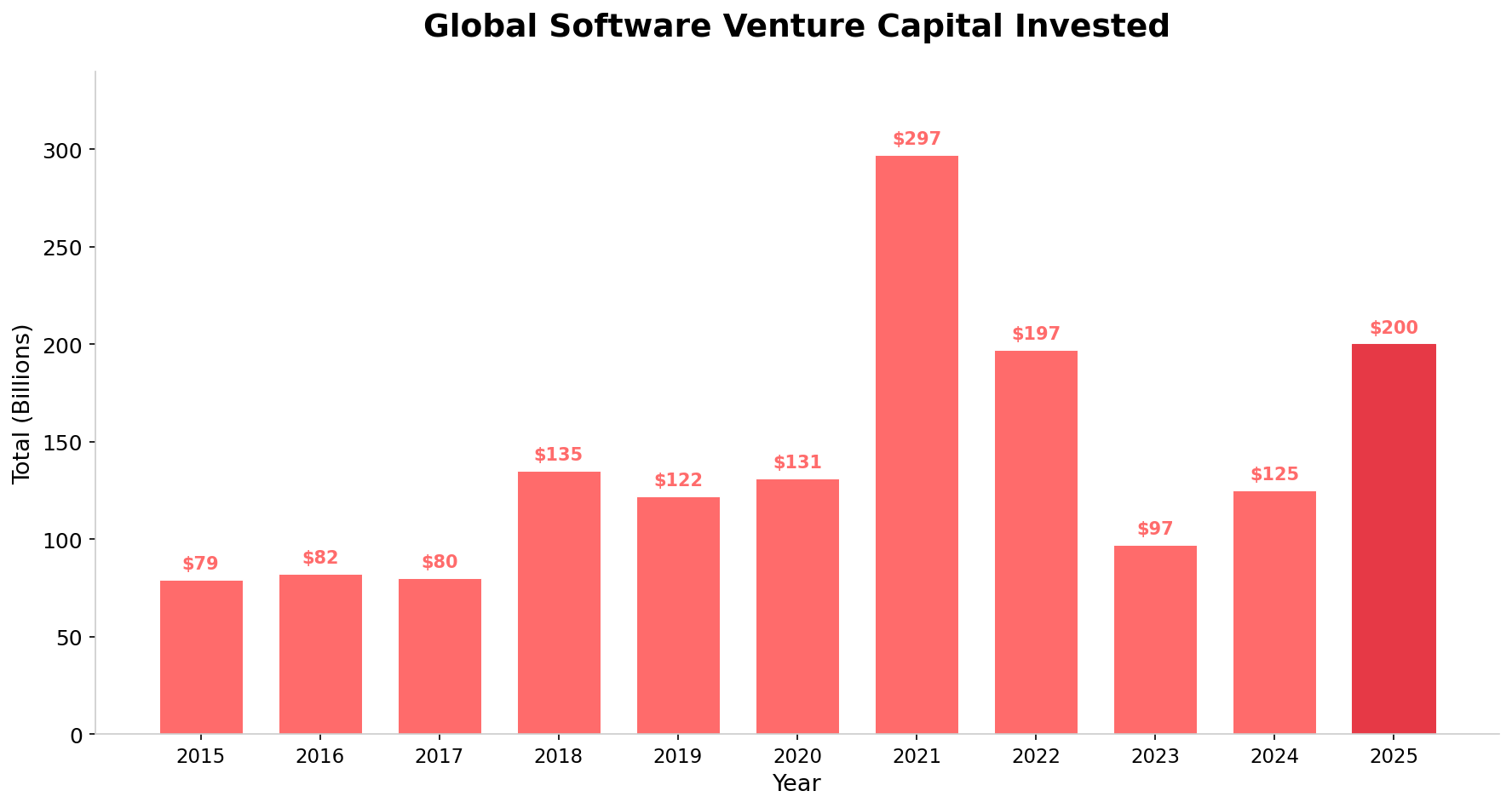

SaaS VC Dollars Invested By Year

Total software VC invested globally reached an estimated $200 billion in 2025, up 60% from $125 billion in 2024 and the second-highest annual total ever, behind only the $297 billion peak in 2021.

SaaS VC Dollars Invested By Year

Non-AI software VC investment remained relatively flat at roughly $95 billion, meaning the headline growth was almost entirely AI-driven. For SaaS founders, the implication is stark: integrating AI into your product strategy has become table stakes for attracting venture investment.

Global Software VC Invested By Round

| Year | Seed | Series A | Series B | Series C | Series D+ | Total |

|---|---|---|---|---|---|---|

| 2025 | $17.5B | $35.0B | $24.5B | $38.0B | $85.0B | $200B |

| 2024 | $15.7B | $26.4B | $17.6B | $30.0B | $35.4B | $125B |

| 2023 | $17.9B | $24.8B | $9.8B | $17.3B | $27.0B | $97B |

| 2022 | $28.5B | $49.7B | $21.8B | $38.2B | $58.5B | $197B |

| 2021 | $22.0B | $54.2B | $32.7B | $64.7B | $123.2B | $297B |

| 2020 | $11.7B | $30.1B | $11.6B | $24.5B | $53.0B | $131B |

The most striking change in 2025 was the explosion in Series D/E/F+ investment, surging to $85 billion — up 140% from $35.4 billion in 2024, driven almost entirely by AI mega-rounds.

How Software Valuations Have Changed

Here are the median pre-money valuations per round over the last twelve years for Series A, B, and C software startups.

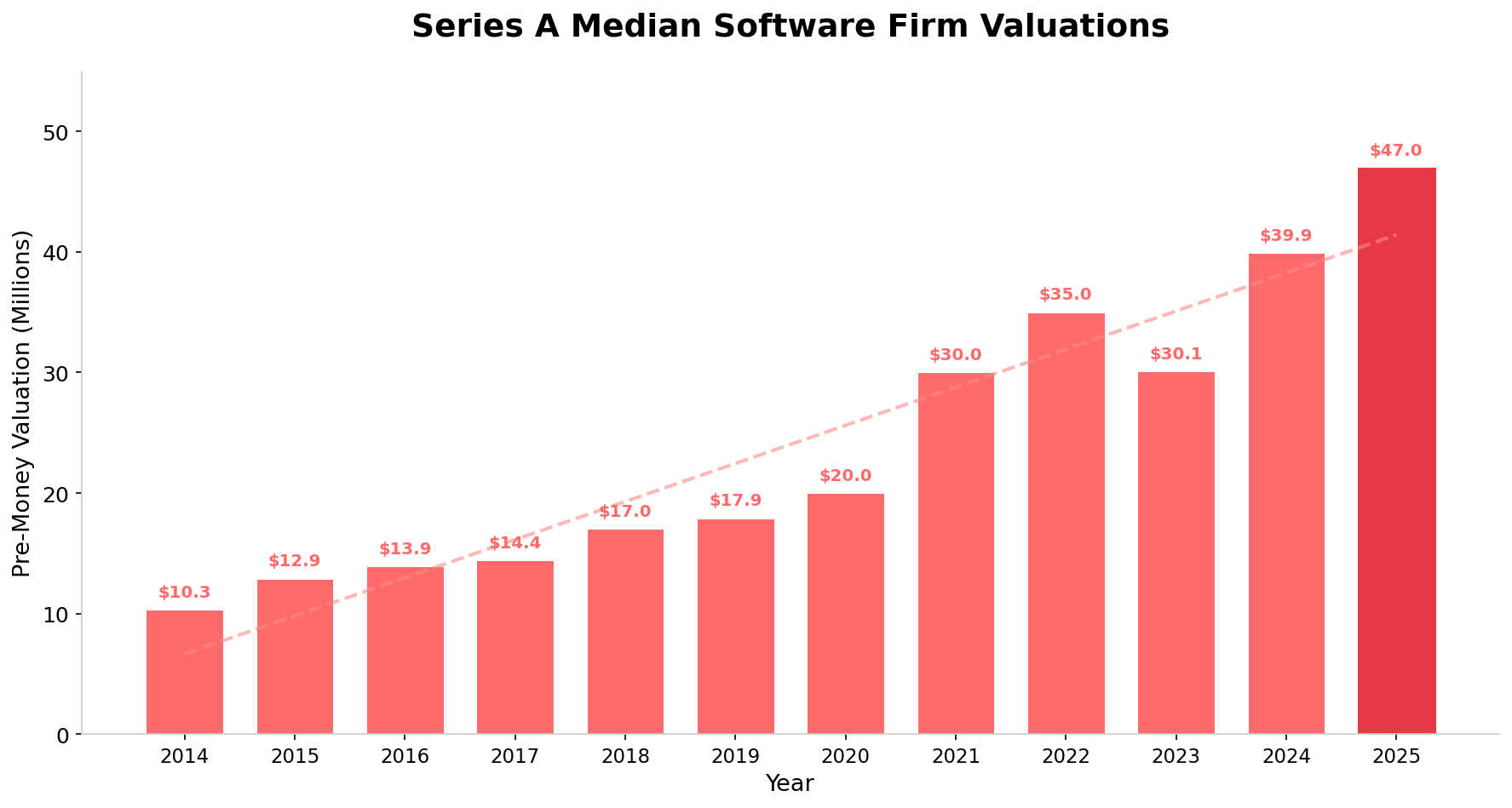

Series A Median Pre-Money Valuations By Year

Series A median pre-money valuations reached a new all-time high of $47.0 million in 2025, up 18% from the previous record of $39.9 million in 2024. AI-native startups are commanding $60-80M+ pre-money valuations at Series A.

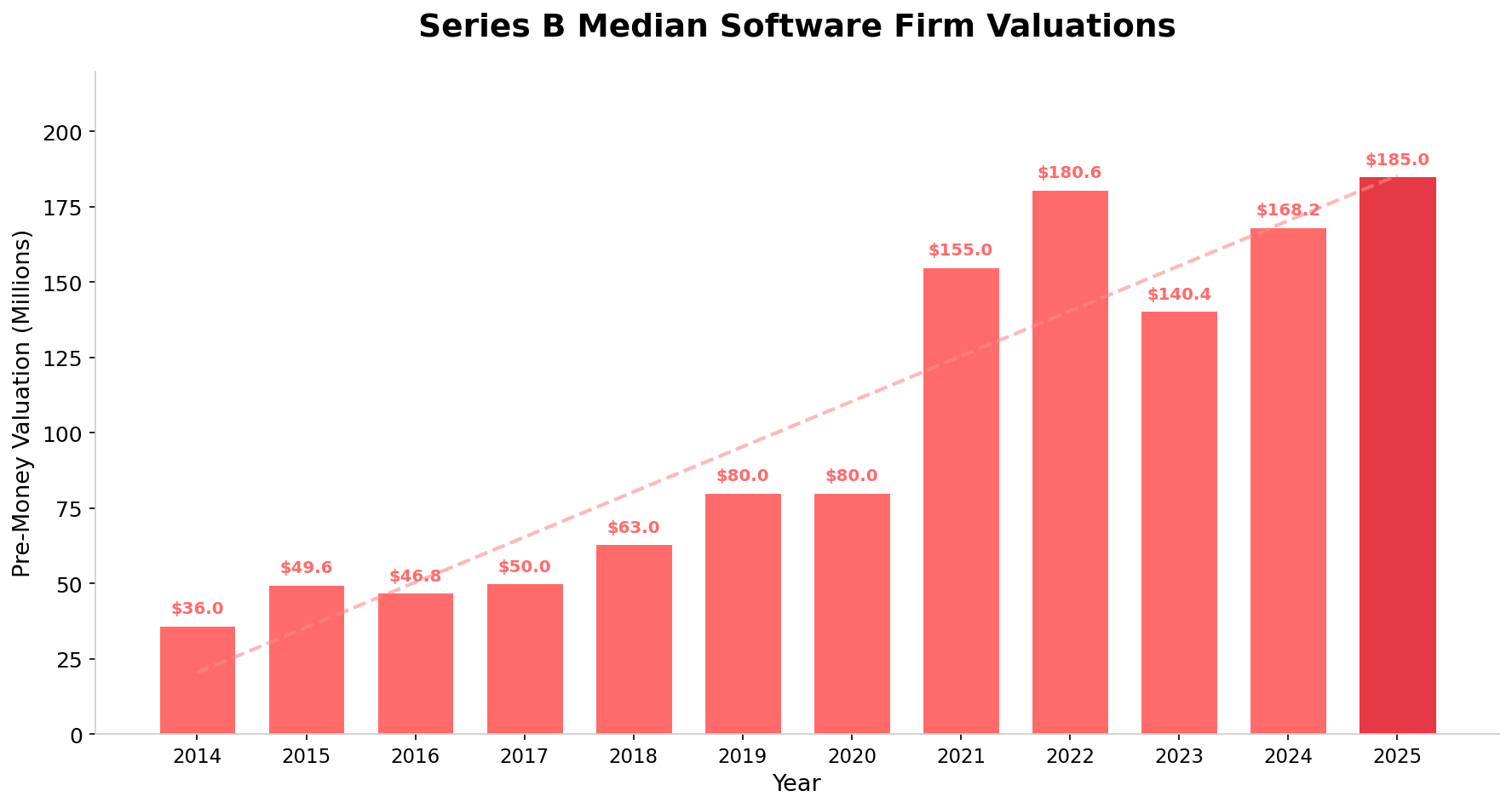

Series B Median Pre-Money Valuations By Year

Series B median pre-money valuations rose to an estimated $185.0 million in 2025, up 10% from $168.2 million in 2024.

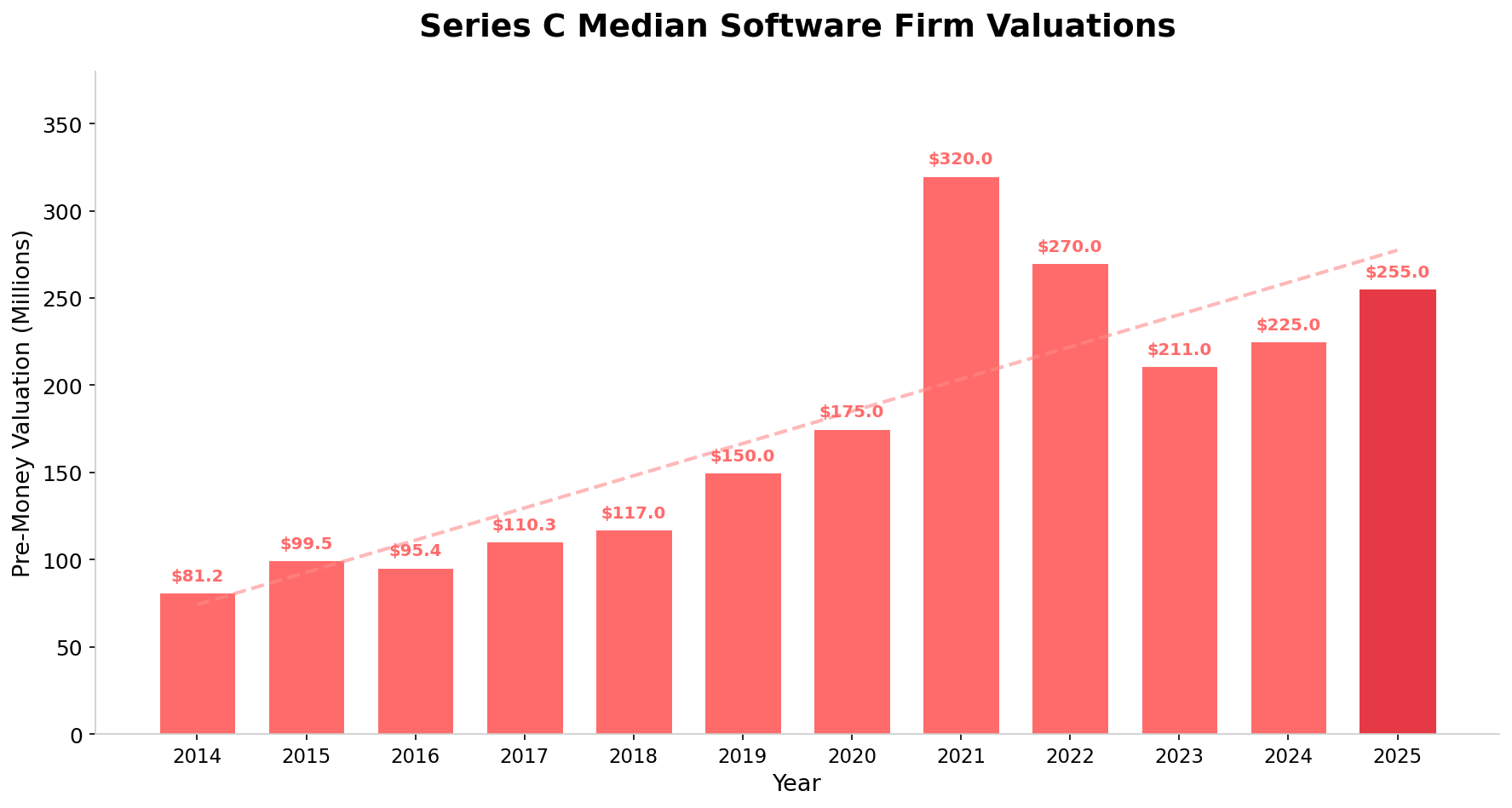

Series C Median Pre-Money Valuations By Year

Series C median pre-money valuations recovered to an estimated $255.0 million in 2025, up 13% from $225.0 million in 2024 but still below the $320 million peak in 2021.

SaaS VC Deal Valuations By Round By Year

| Year | Series A Amount | Series A Val. | Series B Amount | Series B Val. | Series C Amount | Series C Val. |

|---|---|---|---|---|---|---|

| 2025 | $13.5M | $47.0M | $32.0M | $185.0M | $42.0M | $255.0M |

| 2024 | $12.0M | $39.9M | $30.0M | $168.2M | $35.0M | $225.0M |

| 2023 | $10.4M | $30.1M | $28.5M | $140.4M | $30.0M | $211.0M |

| 2022 | $11.4M | $35.0M | $34.0M | $180.6M | $50.0M | $270.0M |

| 2021 | $10.0M | $30.0M | $30.9M | $155.0M | $50.0M | $320.0M |

| 2020 | $7.0M | $20.0M | $20.0M | $80.0M | $30.8M | $175.0M |

| 2019 | $6.6M | $17.9M | $20.0M | $80.0M | $30.0M | $150.0M |

| 2018 | $6.3M | $17.0M | $16.0M | $63.0M | $25.8M | $117.0M |

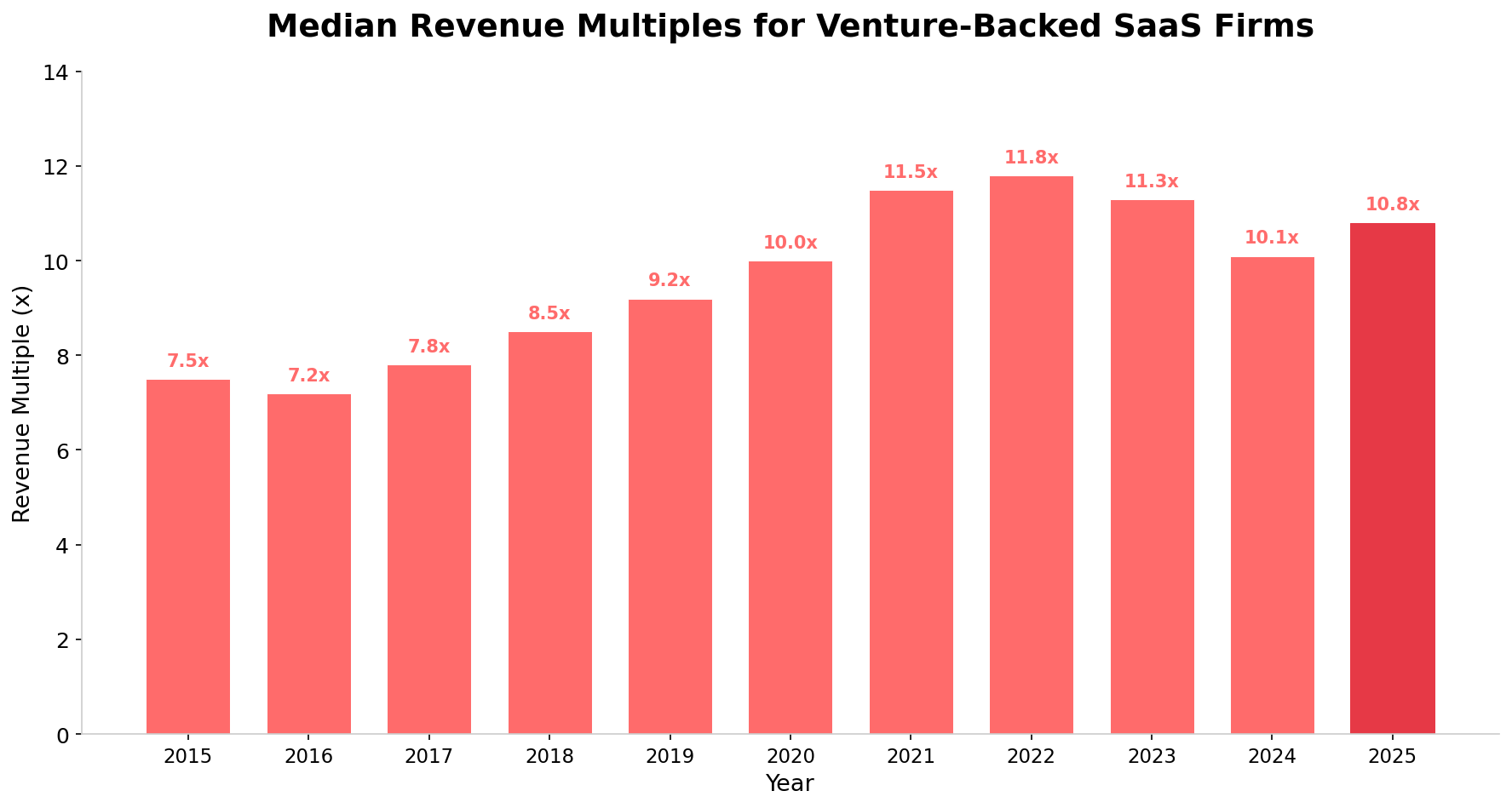

SaaS VC Deal Revenue Multiples

In 2025, the median revenue multiple for venture-backed SaaS companies was approximately 10.8x ARR, up from 10.1x in 2024. AI-powered SaaS companies typically commanded 14-20x+ revenue multiples, while traditional SaaS companies without an AI narrative saw multiples compress to 6-8x.

SaaS Revenue Multiples By Year

| Annual Revenue Growth Rate | Median Revenue Multiple (2025) | Change from 2024 |

|---|---|---|

| <20% (Low Growth) | 4.5x | -0.5x |

| 20–40% | 7.2x | -0.3x |

| 40–60% | 9.8x | +0.2x |

| 60–80% | 12.5x | +0.5x |

| 80–100% | 15.0x | +1.0x |

| >100% (Hyper Growth) | 20.0x+ | +2.0x+ |

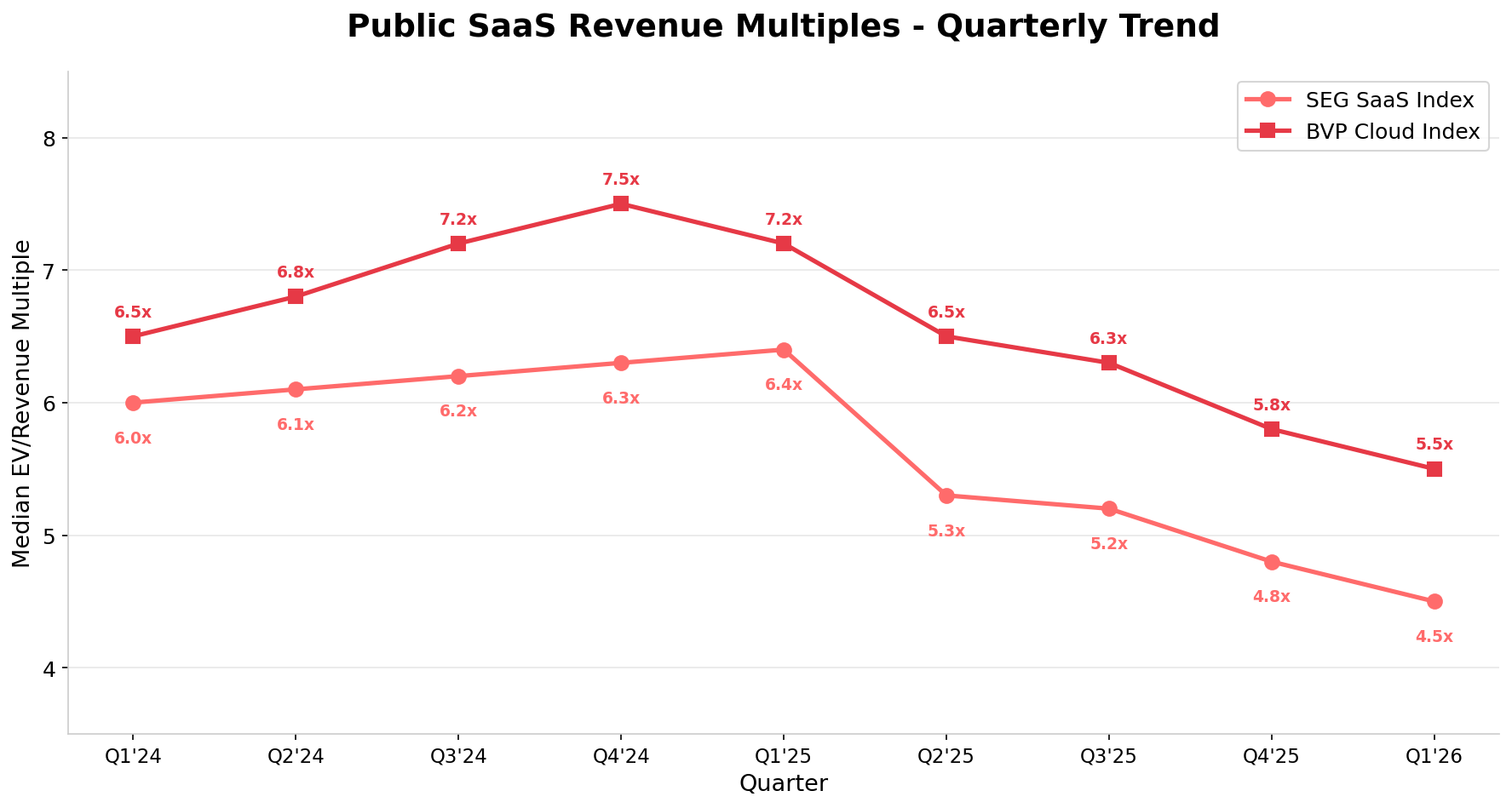

Public SaaS Multiples Under Pressure

While private venture-backed SaaS valuations held up reasonably well in 2025 (boosted by AI), the public SaaS market told a very different story. Public SaaS multiples declined sharply throughout 2025, driven by fears of AI disruption and a rotation toward profitability metrics.

Public SaaS Revenue Multiples – Quarterly Trend (SEG SaaS Index & BVP Cloud Index)

- The SEG SaaS Index declined from 6.3x EV/Revenue (Q4 2024) to 4.8x (Q4 2025) — a 24% decline in one year

- Per Aventis Advisors, the median EV/Revenue for public SaaS fell to 3.4x as of March 2026

- Profitable SaaS companies traded at 7.8x revenue vs. 6.7x for unprofitable peers

- For the first time, EV/EBITDA is becoming the dominant valuation metric for SaaS (~26.6x)

⚠️ The SaaSpocalypse and AI Disruption: Investors are increasingly questioning whether traditional SaaS business models — based on per-seat licensing — will survive the rise of AI agents. This has led to a broad repricing of the sector, with median revenue growth falling to 12.2% by Q4 2025. Companies with clear AI integration stories have been rewarded; those without face existential questions from investors.

| Company Profile | Expected Revenue Multiple (2026) |

|---|---|

| Public SaaS – Median (157 companies) | 4.0x median / 6.6x average |

| Private VC-Backed SaaS (Series A–C) | 5.3x median / 8.0–10.0x top quartile |

| High-Growth SaaS (>40% growth, >120% NRR) | 10.0x – 15.0x |

| AI-Native SaaS (>100% growth) | 15.0x – 25.0x+ |

| Traditional SaaS (<20% growth) | 2.0x – 5.0x |

| SaaS with NRR < 90% | 1.0x – 2.5x |

Hot SaaS Sectors for VC in 2026

- AI Infrastructure & Developer Tools: The hottest sector in 2025. Cursor raised $2.3B at $29.3B valuation. AI coding assistants, vector databases, model serving infrastructure, and AI observability tools dominated.

- AI-Powered Vertical SaaS: Healthcare AI, legal AI, financial AI, and construction/real estate AI attracted premium valuations. Vertical AI delivers immediate, measurable ROI.

- Cybersecurity & Identity: Security maintained premium valuations (6.3x EV/Revenue in Q4 2025). Zero-trust, identity access management, and AI security were key sub-sectors.

- Data Infrastructure & Analytics: The only SEG product category to see multiples expand year-over-year in 2025 (+11% to 4.5x). Databricks' $4B+ Series L at $134B exemplified the space.

- Defense & Government Tech: A breakout category in 2025, led by Anduril's $2.5B Series G.

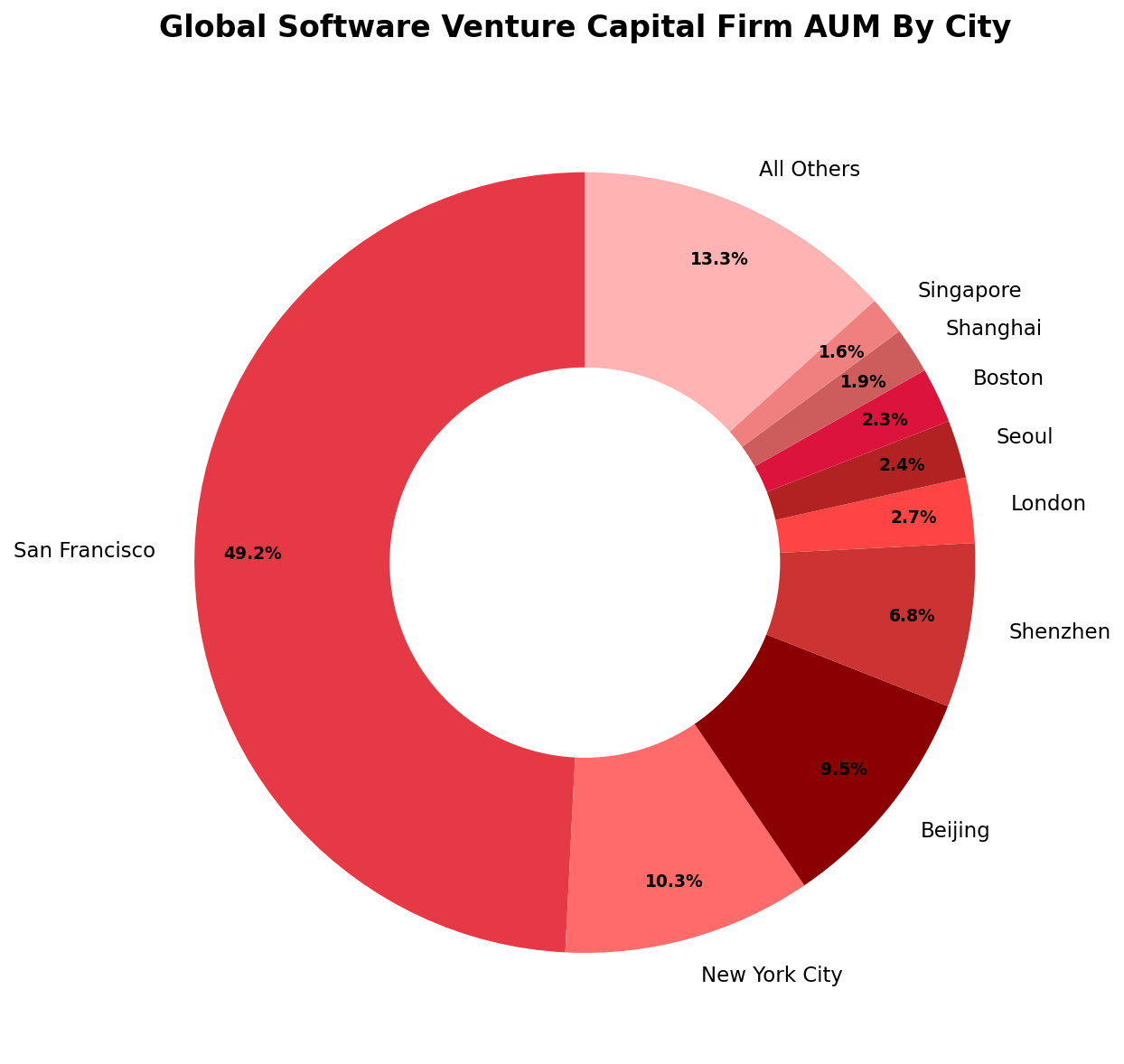

The Best Locations for Software VC

| City | Total AUM (Millions) | % of Total |

|---|---|---|

| San Francisco | 565,200 | 49.2% |

| New York City | 118,450 | 10.3% |

| Beijing | 109,250 | 9.5% |

| Shenzhen | 78,200 | 6.8% |

| London | 31,050 | 2.7% |

| Seoul | 27,600 | 2.4% |

| Boston | 26,450 | 2.3% |

| Singapore | 18,400 | 1.6% |

| Tel Aviv | 14,950 | 1.3% |

| All Others | 259,450 | 22.6% |

Top 400 SaaS VC Firms – AUM By City

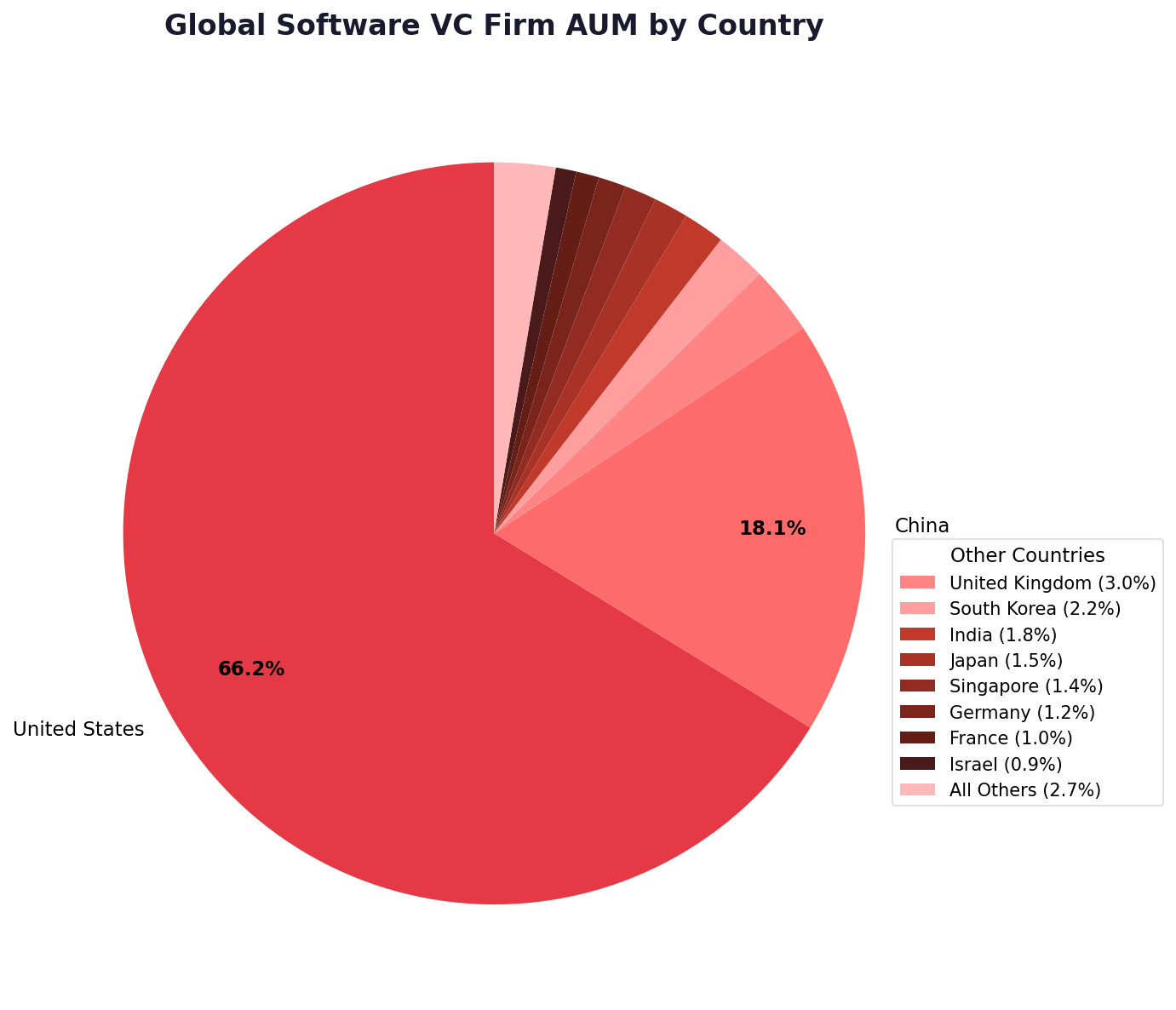

Top 400 SaaS VC Firms – AUM By Country

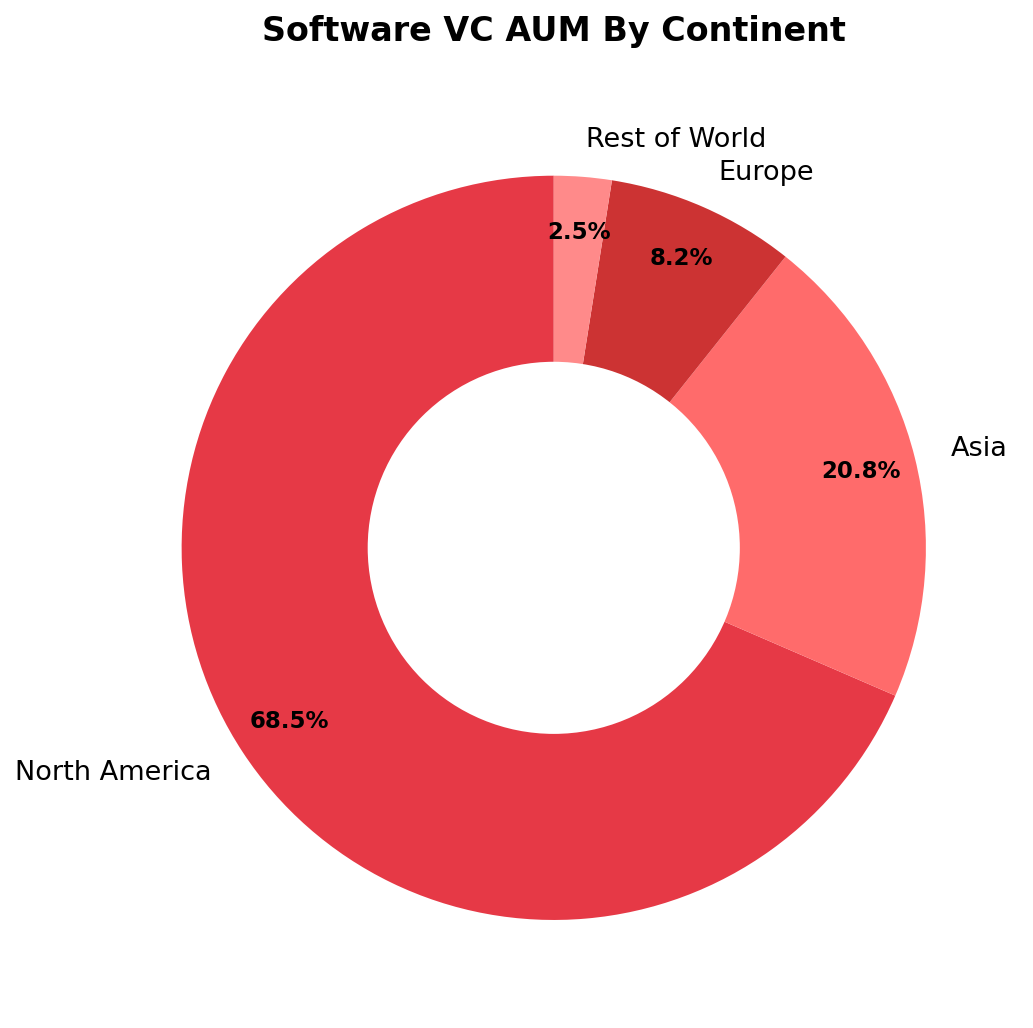

Top 400 SaaS VC Firms – AUM By Continent

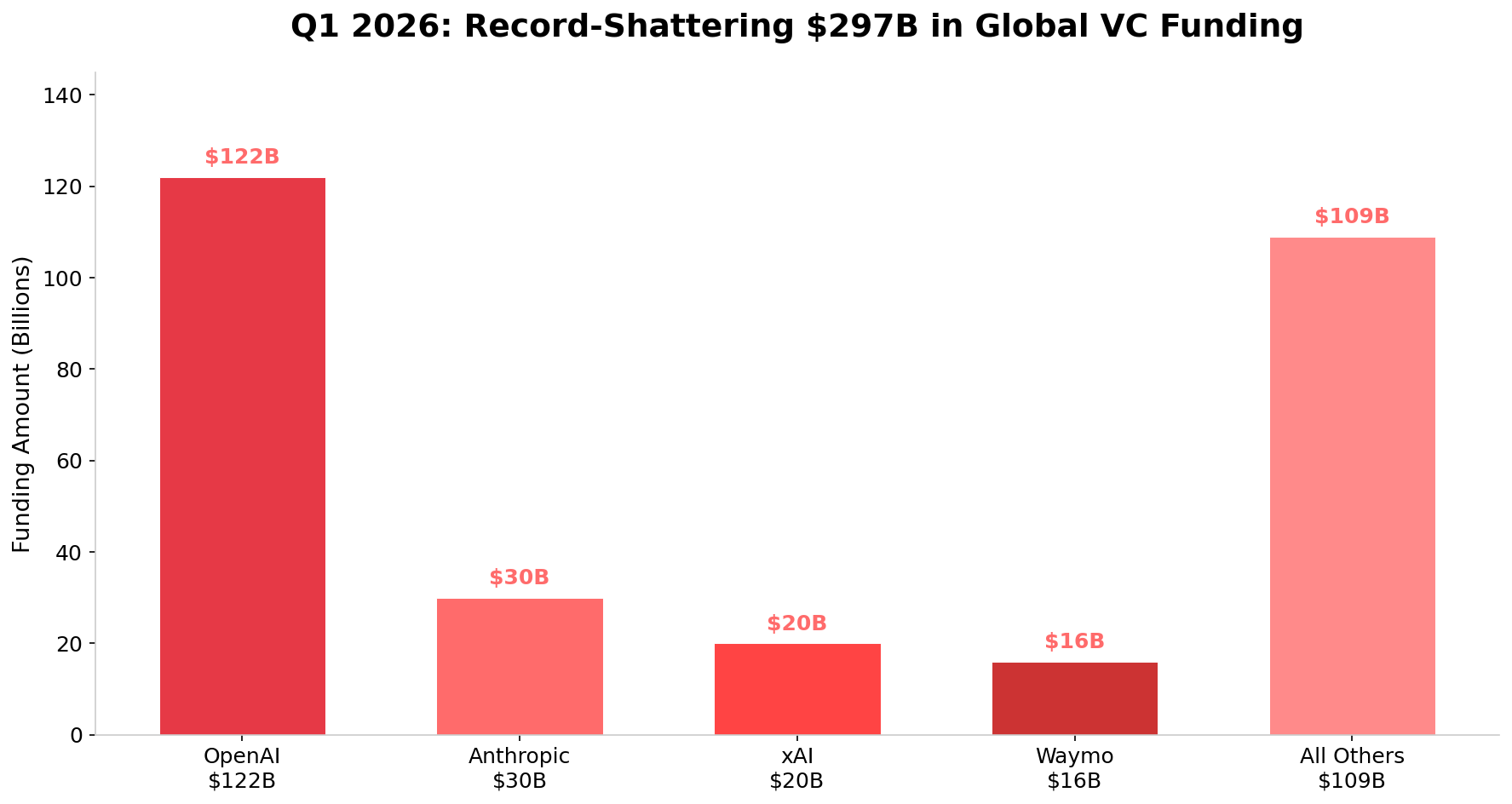

Q1 2026: The Quarter That Broke All Records

$297 billion in global VC funding in Q1 2026 alone — 2.5x the $118B raised in Q4 2025 — more than every full year before 2019.

Q1 2026 VC Mega-Rounds

The unprecedented spike was driven by four behemoth deals:

| Company | Amount | Post-Money Valuation | Key Investors |

|---|---|---|---|

| OpenAI | $122B | $852B | SoftBank, a16z, Amazon, Nvidia, Microsoft |

| Anthropic | $30B | $380B | GIC, Coatue, Founders Fund, ICONIQ |

| xAI | $20B | ~$230B | Valor Equity, Fidelity, QIA, Nvidia |

| Waymo | $16B | $126B | Dragoneer, Sequoia, Alphabet |

These four rounds alone raised $188 billion, accounting for 63% of total Q1 2026 funding. OpenAI's $122 billion round — the largest private funding round in history — valued the company at $852 billion.

SaaS VC Outlook for 2026 and Beyond

- AI Will Continue to Dominate: AI will likely capture 60%+ of software VC dollars in 2026. Investors are increasingly distinguishing genuine AI innovation from "AI-washing."

- The Great SaaS Repricing: Traditional SaaS without clear AI strategies will continue facing valuation pressure. Focus on profitability, efficiency, and Rule of 40.

- Dry Powder Creates Opportunity: Global VC dry powder remains substantial at ~$600 billion. As interest rates normalize, capital should begin flowing more freely.

- The Exit Window Is Opening: 2025 saw exit value surge to $549.2 billion. The IPO market is thawing and the environment is improving for the first time since 2021.

- Profitability Is the New Growth: Profitable SaaS trades at 7.8x vs. 6.7x for unprofitable peers. EV/EBITDA is becoming the primary valuation metric for SaaS.

Our Prediction: We expect total software VC investment to reach $250–300 billion in 2026, potentially matching the 2021 record. AI mega-rounds will continue to dominate headline numbers, but we also expect a recovery in traditional SaaS investment as the exit window opens and SaaS companies increasingly integrate AI.

Want to connect with other SaaS CEOs navigating this landscape? Join 400+ SaaS founders at SaasRise.

Apply to Join SaasRise →Sources & Methodology

This report draws on data from the following sources, all accessed and verified in March–April 2026:

- PitchBook-NVCA Venture Monitor (Q4 2025) — US VC deal activity, AI/ML deal share (65.6%), valuations

- KPMG Venture Pulse (Q4 2025) — Quarterly global VC investment, exit value, fundraising

- TechCrunch / Crunchbase — Q1 2026 Record Quarter ($297B)

- SEG 2026 Annual SaaS Report — SEG SaaS Index quarterly medians (Q4'24: 6.3x → Q4'25: 4.8x)

- BVP Nasdaq Emerging Cloud Index — Average revenue multiple (5.8x)

- Aventis Advisors — SaaS Valuation Multiples 2015–2026, median EV/Revenue (3.4x as of March 2026)

- SaaS Capital Index — Median public SaaS ARR multiple

- OpenAI — $122B at $852B valuation (March 2026)

- Anthropic — $30B Series G at $380B (Feb 2026)

- xAI — $20B Series E at ~$230B (Jan 2026)

- Waymo — $16B at $126B (Feb 2026)

- Databricks — $4B+ Series L at $134B (Dec 2025)

- S&P Capital IQ, PitchBook, CB Insights — Deal data and market analytics

Rise Worldwide, Inc. | 3609 Country White Lane, Austin, TX 78749