The SaaS M&A Report 2026

Mergers, Acquisitions, Valuations & The SaaSpocalypse

A comprehensive analysis of SaaS deal activity, valuations, and the AI disruption reshaping the industry

Executive Summary

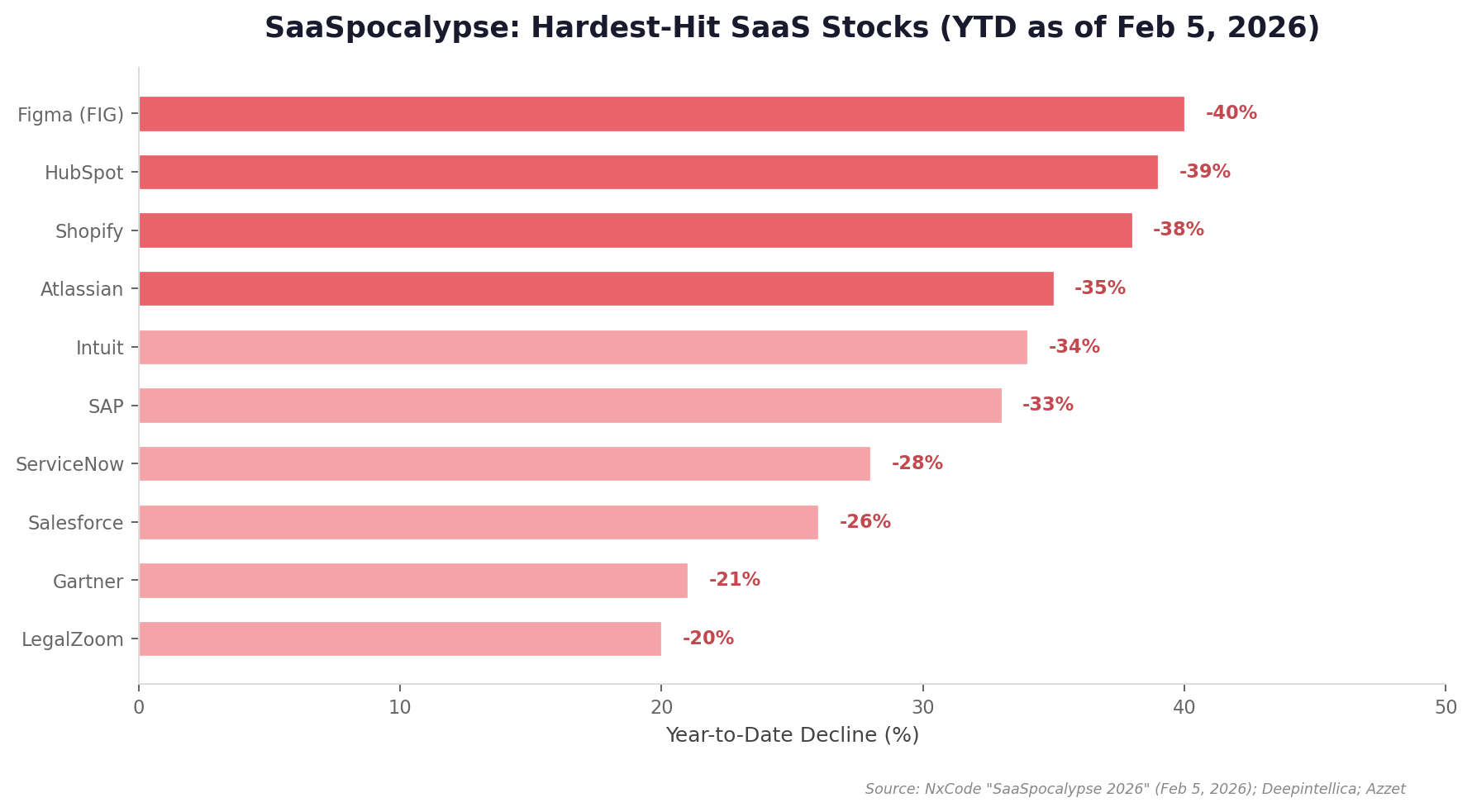

The SaaS industry entered 2026 in the grip of its most significant market disruption since the 2022 rate-hike correction. What Wall Street traders dubbed the "SaaSpocalypse"—triggered by Anthropic's launch of Claude Cowork on January 12, 2026—erased approximately $1 trillion in aggregate market capitalization from enterprise SaaS stocks in just weeks.

Yet beneath the panic lies a more nuanced story. While public SaaS multiples compressed from ~7.0x to ~5.5x and individual stocks like HubSpot fell 39%, the underlying M&A market remained remarkably active. 2025 set records for SaaS deal volume, with 17 mega-deals exceeding $2.5 billion and total announced deal value surpassing $180 billion. Cybersecurity and AI infrastructure dominated.

This report covers the full landscape: the record-breaking M&A deals of 2025, the SaaSpocalypse and what it means for valuations, private SaaS multiples entering Q1 2026, the Rule of 40 as the defining metric of this era, and the upcoming mega-IPOs from Anthropic, OpenAI, and SpaceX that will reshape capital markets for years to come.

If you like data-driven SaaS content like this and want more, apply to join the SaasRise mastermind community.

🔥 The SaaSpocalypse: Real or Imagined? NEW

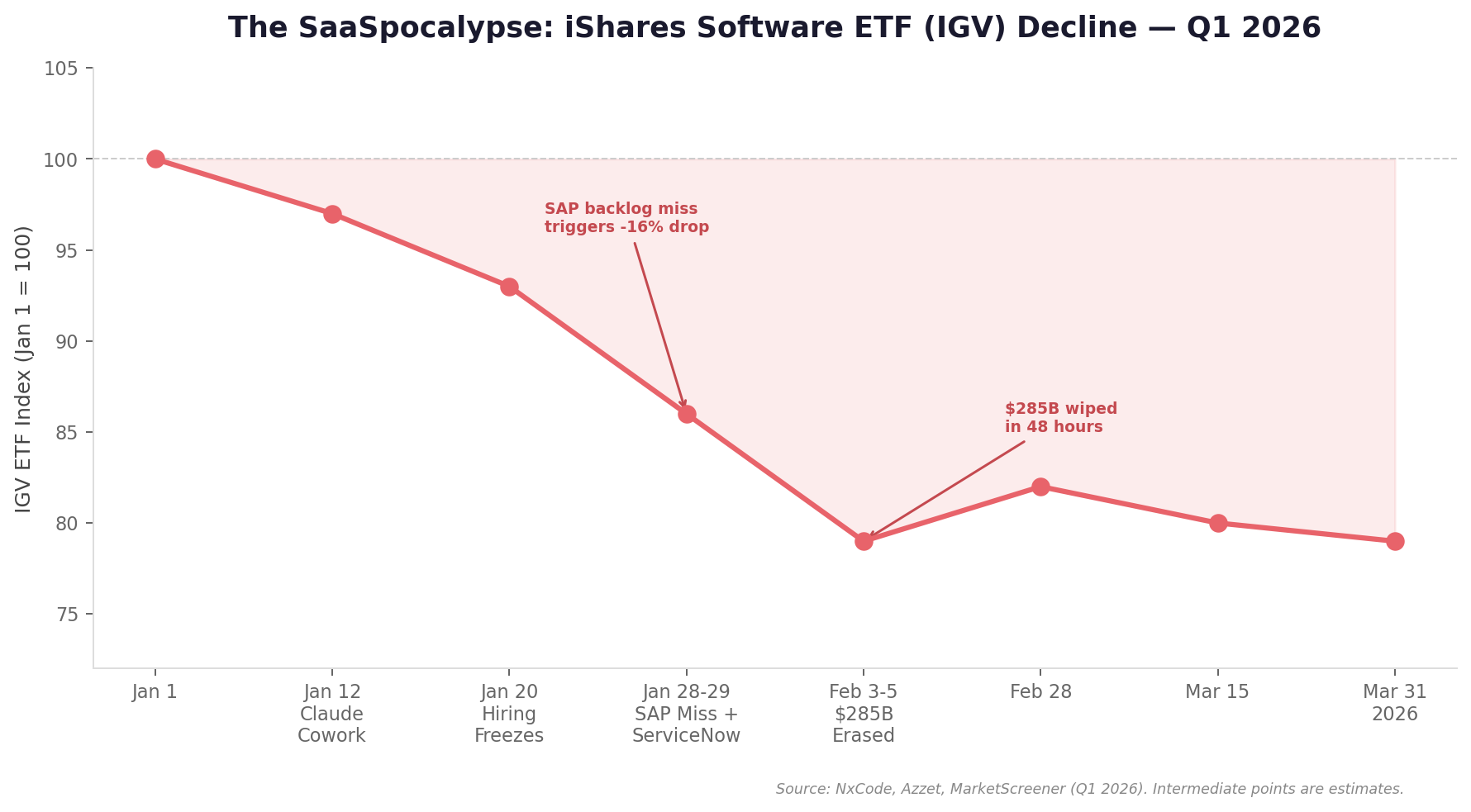

On January 12, 2026, Anthropic launched Claude Cowork—an autonomous AI agent capable of performing end-to-end business workflows. A journalist built a complete kanban board in under 10 minutes and posted a video. Monday.com's market cap dropped $300 million before the session closed.

What followed was the sharpest software sell-off since the 2000 dot-com crash. Jefferies equity trader Jeffrey Favuzza coined "SaaSpocalypse" and described trading as "very much 'get me out' style selling"—language not heard since 2008.

The Damage: By the Numbers

| Metric | Value |

|---|---|

| Total Market Cap Lost (48 hours) | $285 billion |

| Broader SaaS Losses (Jan–Mar 2026) | ~$1–2 trillion |

| iShares Software ETF (IGV) YTD | Down 21%+ |

| JPMorgan US Software Index | Dropped 7% in a single day |

| Median SaaS Revenue Multiple | Fell from ~7.0x to ~5.5x (SCI) / below 5x (broad) |

| IGV vs 200-Day Moving Average | Widest gap since dot-com crash |

What Actually Triggered the Sell-Off?

The SaaSpocalypse wasn't caused by a single event but a cascade of three converging forces:

- AI Agent Demonstrations (Jan 12–16): Claude Cowork's launch covering 11 business categories proved AI could replicate core SaaS functionality end-to-end. Atlassian and Asana dropped ~4% immediately.

- Disappointing Q4 2025 Earnings (Jan 20–29): Multiple SaaS companies reported slowing growth as customers were reducing seats, not adding them. ServiceNow's earnings call acknowledged "AI substitution risk" for the first time—the stock dropped 11% in the session.

- Wall Street Repricing (Feb 3–5): The February flash crash erased $285B in 48 hours as institutional investors simultaneously realized AI productivity gains were accruing to end users and AI model providers—not to SaaS vendors.

Bain & Company (Feb 9, 2026): "The sharp declines in public software values reflect rising concerns over AI's growing ability to replicate core functionality and, over time, erode installed bases. Broad software indices are now down by about 15% over the past few weeks and by about 25% from 12-month highs."

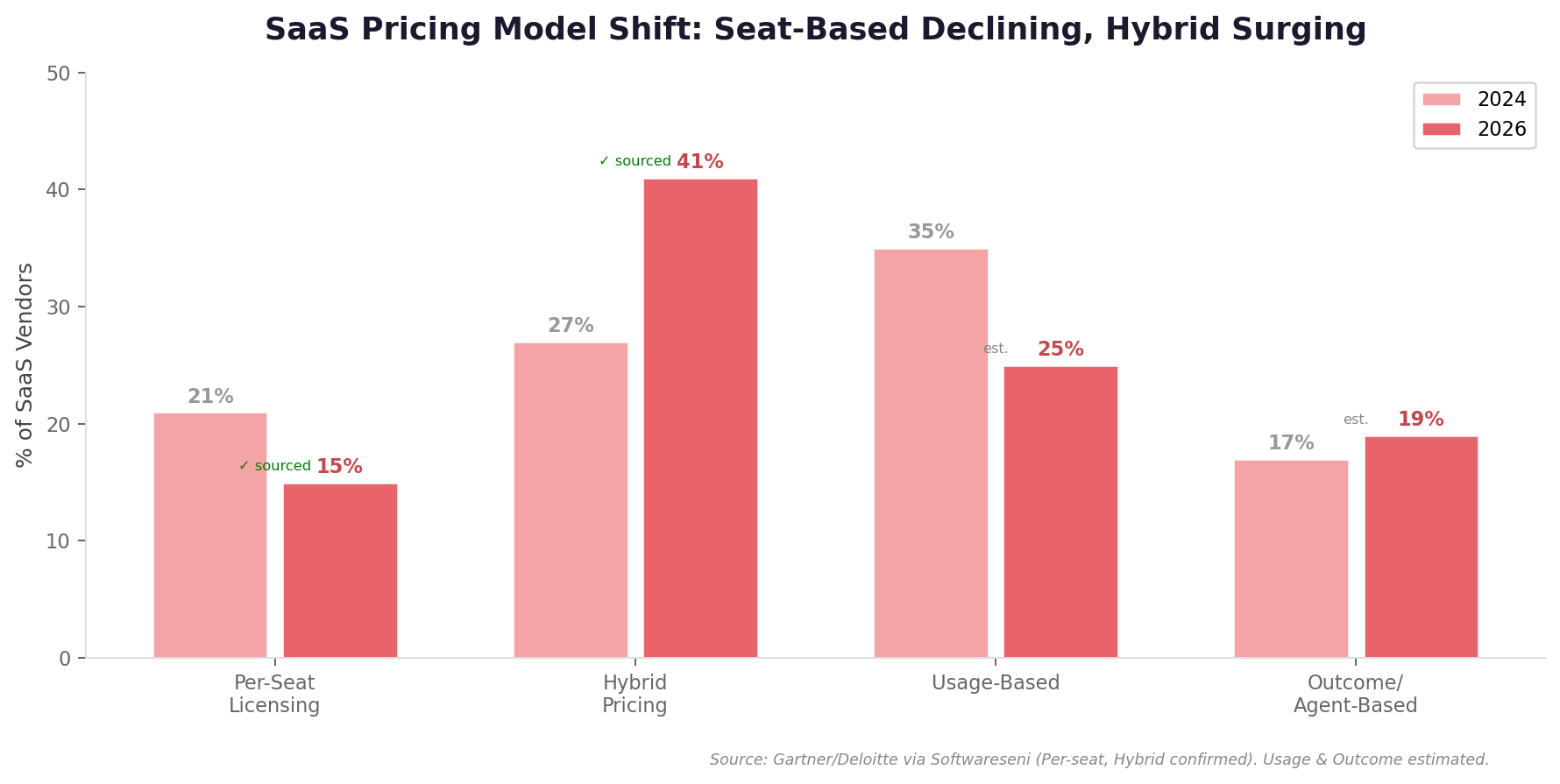

The "Seat Compression" Thesis

The core fear driving the sell-off is simple math: if 10 AI agents replace 100 employees, a company needs 10 software seats instead of 100—a 90% revenue reduction. Bank of America called the sell-off "internally inconsistent" because investors can't simultaneously believe AI capex will fail and that AI will disrupt all software. But the market doesn't always care about internal consistency.

The data shows this is already happening:

- Per-seat pricing fell from 21% to 15% of vendors as a primary model within twelve months

- Hybrid pricing surged from 27% to 41%

- Gartner predicts at least 40% of enterprise SaaS spend will shift to usage-, agent-, or outcome-based pricing by 2030

Is the SaaSpocalypse Real?

Our analysis suggests the truth lies between the extremes:

🔴 Real: The growth assumptions that justified 20–40x revenue multiples are no longer credible. AI budgets are up 100%+ year-on-year while overall IT budgets are up ~8%. AI is absorbing the growth margin from total IT spend—and that margin was previously flowing into SaaS expansion.

🟢 Exaggerated: SaaS products still work. Contracts still renew. Average gross retention is still ~90%. Enterprise systems of record (ERP, core financial platforms) retain strong moats through deep integration and switching costs. Not all software faces the same risk or timeframe.

📊 Our Prediction: Public SaaS multiples will likely stabilize in the 5.0x–6.5x range through the rest of 2026, with a wide bifurcation between AI-native leaders (10x+) and vulnerable horizontal point-solution SaaS (2–4x). The repricing is structural, not a panic that reverses. But the bottom is likely in or near.

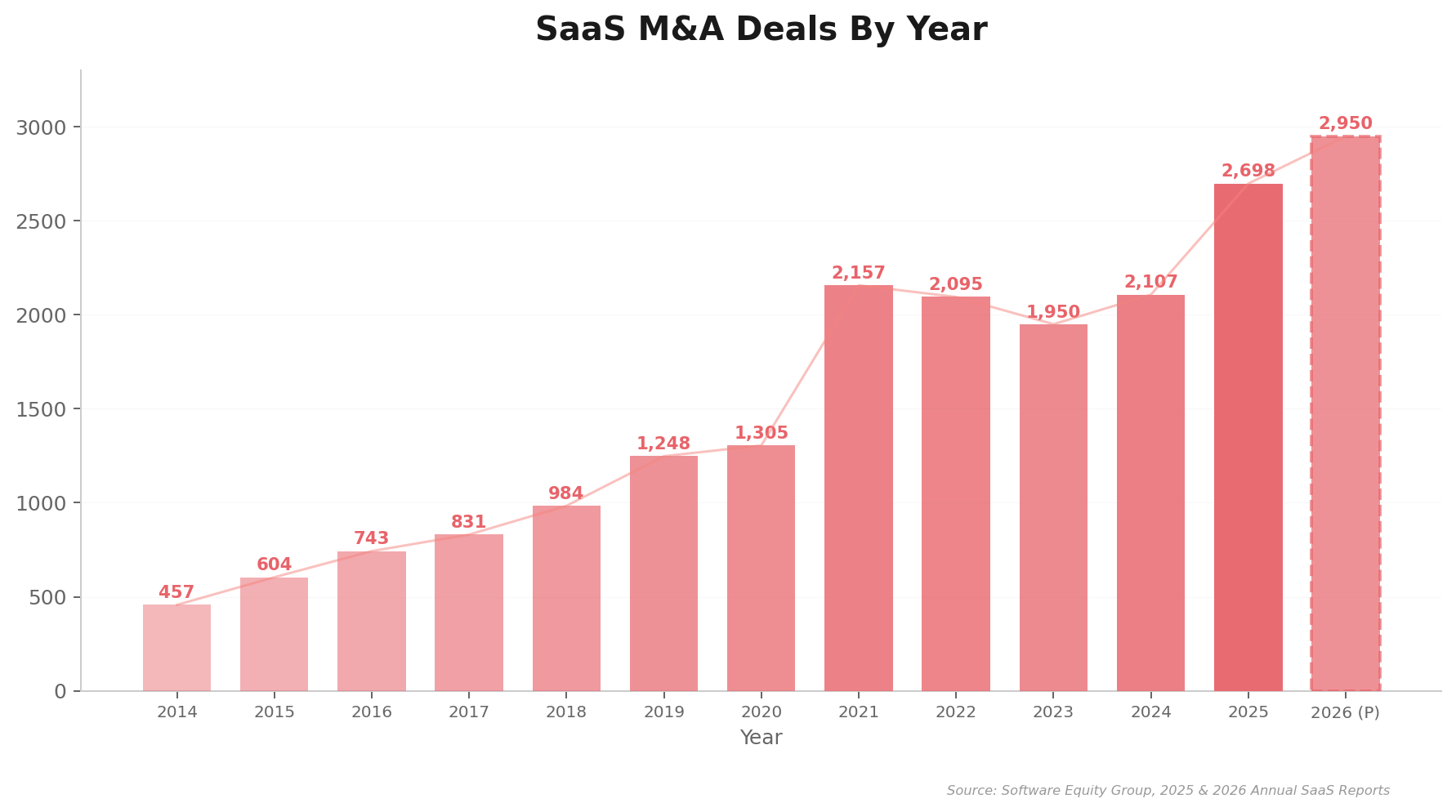

2025 Set an All-Time Record for SaaS M&A Deal Volume

Total SaaS M&A deal volume in 2025 reached record levels with 2,698 SaaS transactions (per Software Equity Group), a 28% increase over 2024's 2,107 deals. Several macro factors drove this surge:

- Record PE dry powder: Over $2.5 trillion in private equity capital seeking deployment

- Lower interest rates: The Fed's rate-cutting cycle that began in late 2024 continued through 2025

- AI urgency: Strategic acquirers racing to add AI capabilities before competitors

- Regulatory clarity: The clearance of HPE/Juniper and Google/Wiz emboldened boards

The Top Private & Public M&A Exits of 2025

Despite market turbulence, 2025 was a record-setting year for SaaS M&A. We tracked 17 mega-deals exceeding $2.5 billion, led by Google's $32 billion acquisition of Wiz—the largest pure-play SaaS acquisition in history. Cybersecurity dominated with four of the top deals.

| # | Acquirer | Target | Deal Value | Date | Type |

|---|---|---|---|---|---|

| 1 | Alphabet (Google) | Wiz | $32.0B | Mar 2025* | Cybersecurity |

| 2 | Palo Alto Networks | CyberArk | $25.0B | Jul 2025 | Identity Security |

| 3 | Meta | Scale AI (49% stake) | $14.3B | Jun 2025 | AI Data / Acqui-hire |

| 4 | HPE | Juniper Networks | $14.0B | Jul 2025** | Networking / AI |

| 5 | Thoma Bravo | Dayforce (Ceridian) | $12.3B | Aug 2025 | HR / Payroll |

| 6 | IBM | Confluent | $11.0B | Dec 2025* | Data Streaming |

| 7 | CoreWeave | Core Scientific | $9.0B | Jul 2025 | AI Infrastructure |

| 8 | Vista + Blackstone | Smartsheet | $8.4B | Jan 2025 | Work Management |

| 9 | Salesforce | Informatica | $8.0B | May 2025 | Data Management |

| 10 | ServiceNow | Armis | $7.75B | Dec 2025 | Cybersecurity / IoT |

| 11 | OpenAI | io Products (Jony Ive) | $6.5B | May 2025 | AI Hardware |

| 12 | Clearlake Capital | ModMed | $5.3B | Mar 2025 | Healthcare IT |

| 13 | AMD | ZT Systems | $4.9B | Mar 2025** | AI Infrastructure |

| 14 | Palo Alto Networks | Chronosphere | $3.35B | Nov 2025* | Observability |

| 15 | Capgemini | WNS | $3.3B | Oct 2025 | BPO / AI Ops |

| 16 | OpenAI | Windsurf (Codeium) | $3.0B | May 2025 | AI Dev Tools |

| 17 | ServiceNow | Moveworks | $2.85B | Mar 2025 | AI Enterprise |

* Deal announced in 2025, closed in early 2026. ** Deal announced prior to 2025, closed in 2025.

Early 2026 Deals Already Announced

The M&A momentum has carried into 2026, with several blockbuster deals announced or completed in Q1 alone:

| Acquirer | Target | Deal Value | Date | Sector |

|---|---|---|---|---|

| Alphabet (Google) | Wiz | $32.0B | Mar 2026 | Cybersecurity |

| IBM | Confluent | $11.0B | Jan 2026 | Data Streaming |

| SoftBank | DigitalBridge | ~$8.5B | Jan 2026 | Data Center Infra |

| ServiceNow | Armis | $7.75B | Jan 2026 | Cyber-Exposure |

| Hg Capital | OneStream | $6.4B | Jan 2026 | Finance / CPM |

| Capital One | Brex | $5.15B | Jan 2026 | Fintech / Payments |

| Meta | Manus | ~$2.0B | Jan 2026 | AI Agents |

Takeaways from All Private Software M&A Transactions in 2025

Based on our analysis of private software M&A transactions...

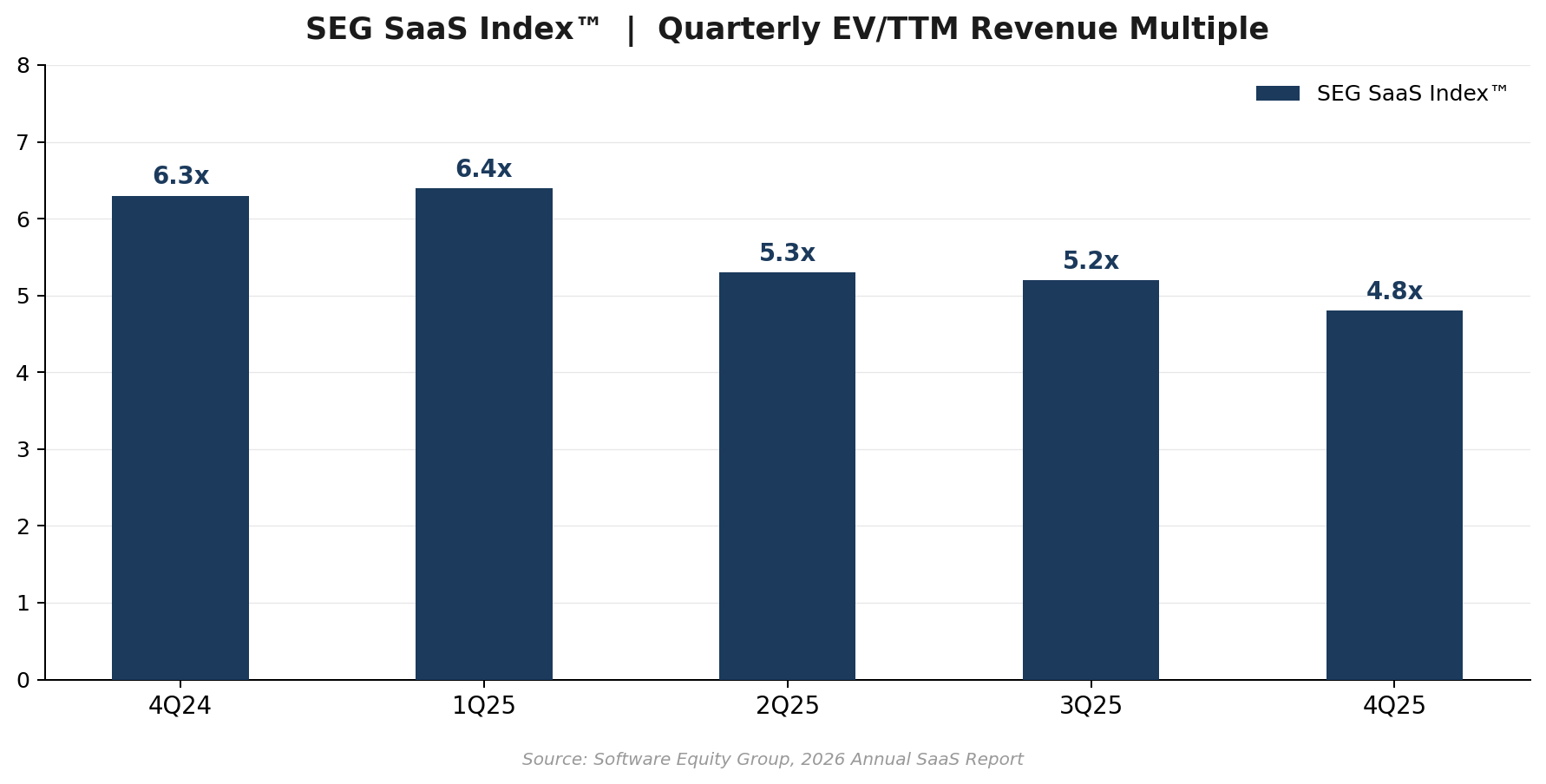

(PUBLIC SAAS, Q1 '26)

(PUBLIC SAAS, Q1 '26)

(PRIVATE SAAS M&A, Q1 '26)

Key findings from private M&A transactions:

- Deal size is the single strongest predictor of valuation multiples—the median multiple was nearly 2x higher for deals in the $50–100M range vs. $20–50M.

- AI-native companies commanded 40–80% valuation premiums over comparable traditional SaaS.

- Profitability matters more than ever: Investors demand concrete 24-month paths to EBITDA positive; patient capital has disappeared.

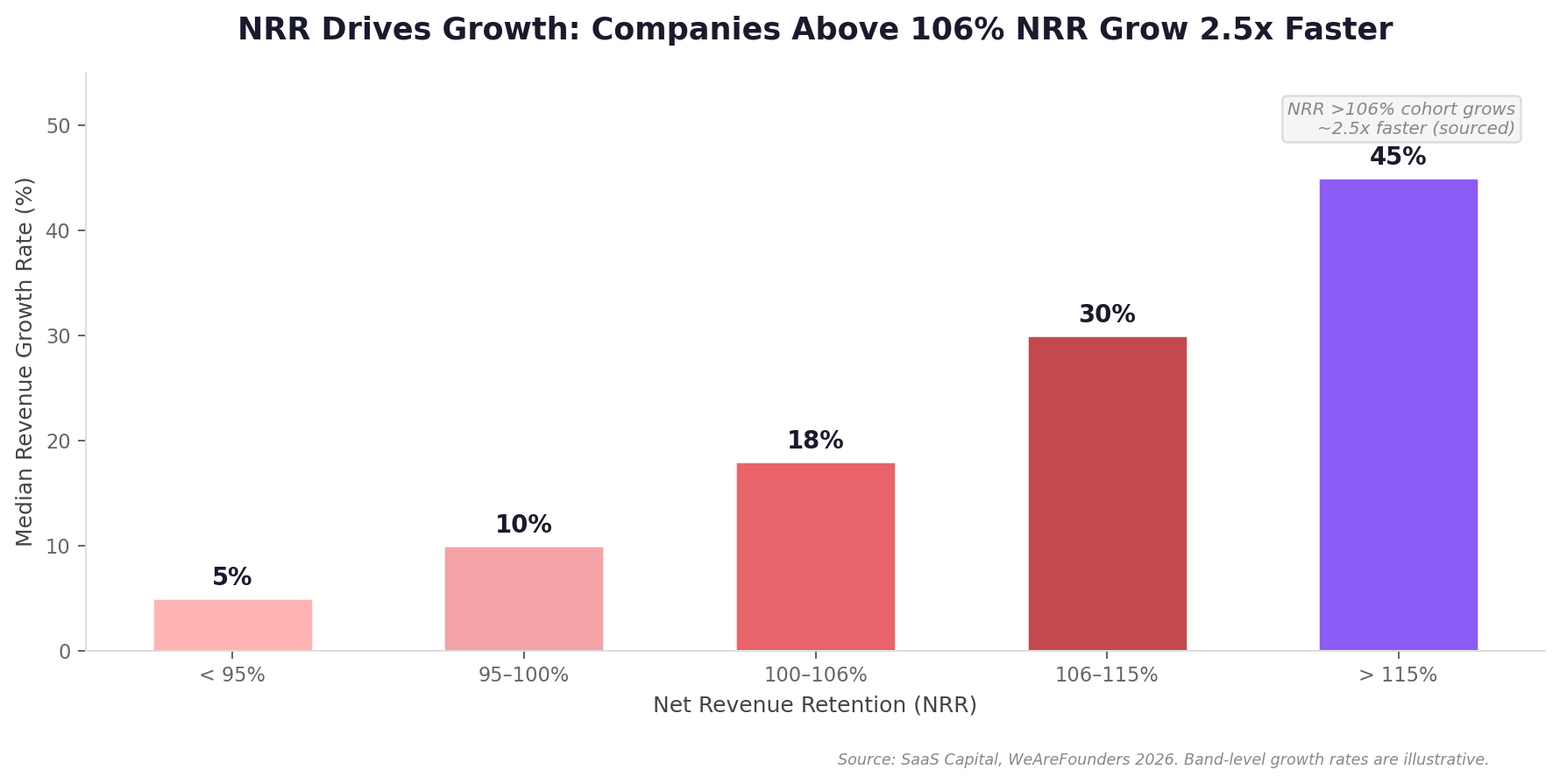

- NRR above 106% correlates with 2.5x faster growth, leading to significantly higher multiples.

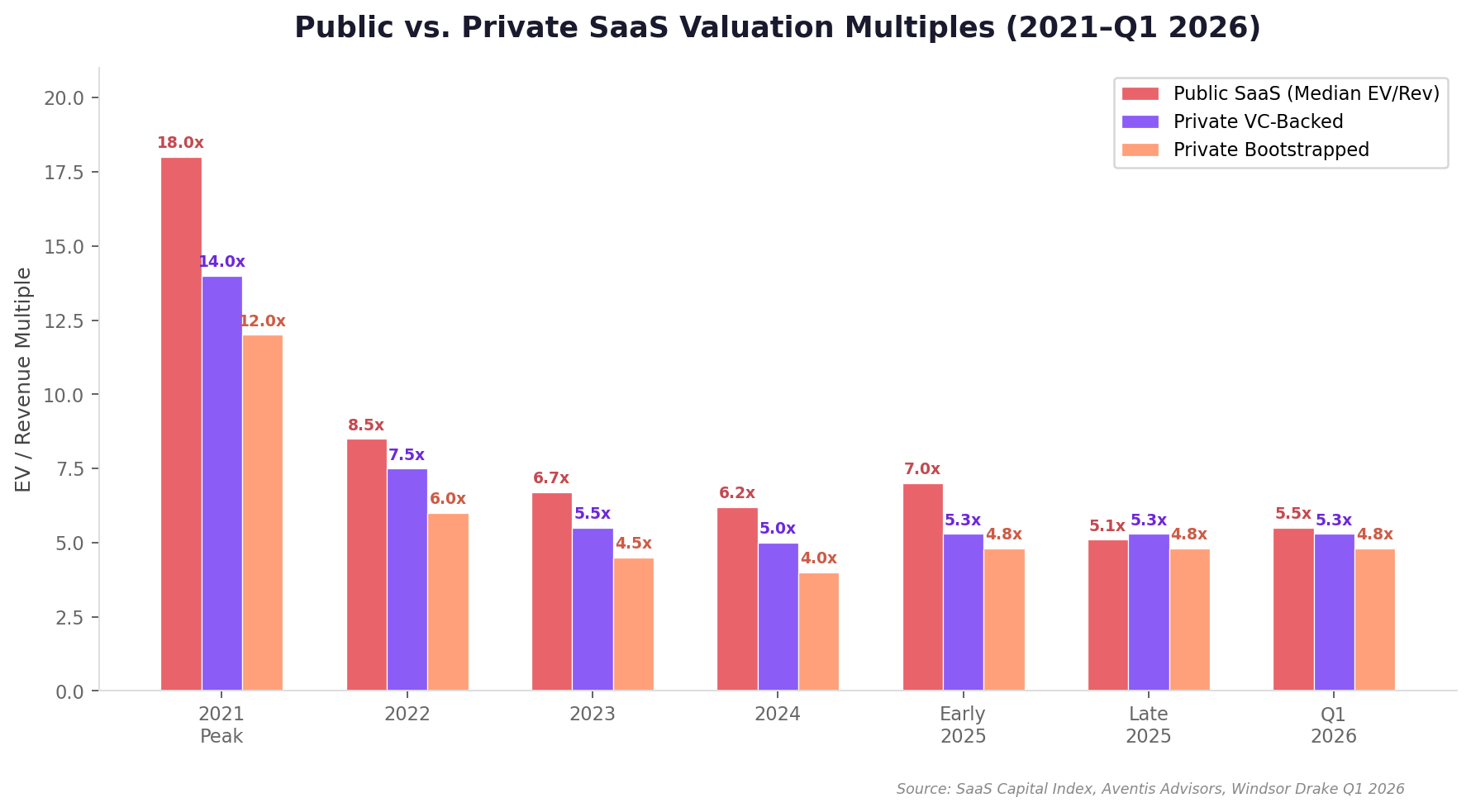

Public vs. Private SaaS Valuations: Q1 2026 NEW

The SaaSpocalypse hit public SaaS valuations hard, but private market multiples have been more resilient. Here's how the landscape looks entering Q1 2026:

| Segment | Median Multiple | Top Quartile | Change vs. 2024 |

|---|---|---|---|

| Public SaaS (SCI, 102 companies) | 5.5x | 12.0–14.5x | 🔴 Down from 7.0x |

| Public SaaS (Broad, 157 companies) | 4.0x median / 6.6x avg | 12.0–14.5x | 🔴 Significant decline |

| Private VC-Backed (Series A–C) | 5.3x | 8.0–10.0x | 🟡 Stable |

| Private Bootstrapped | 4.8x | 6.0x | 🟡 Stable |

| AI-Native / Vertical SaaS | 9.0–12.0x | 15.0x+ | 🟢 Premium growing |

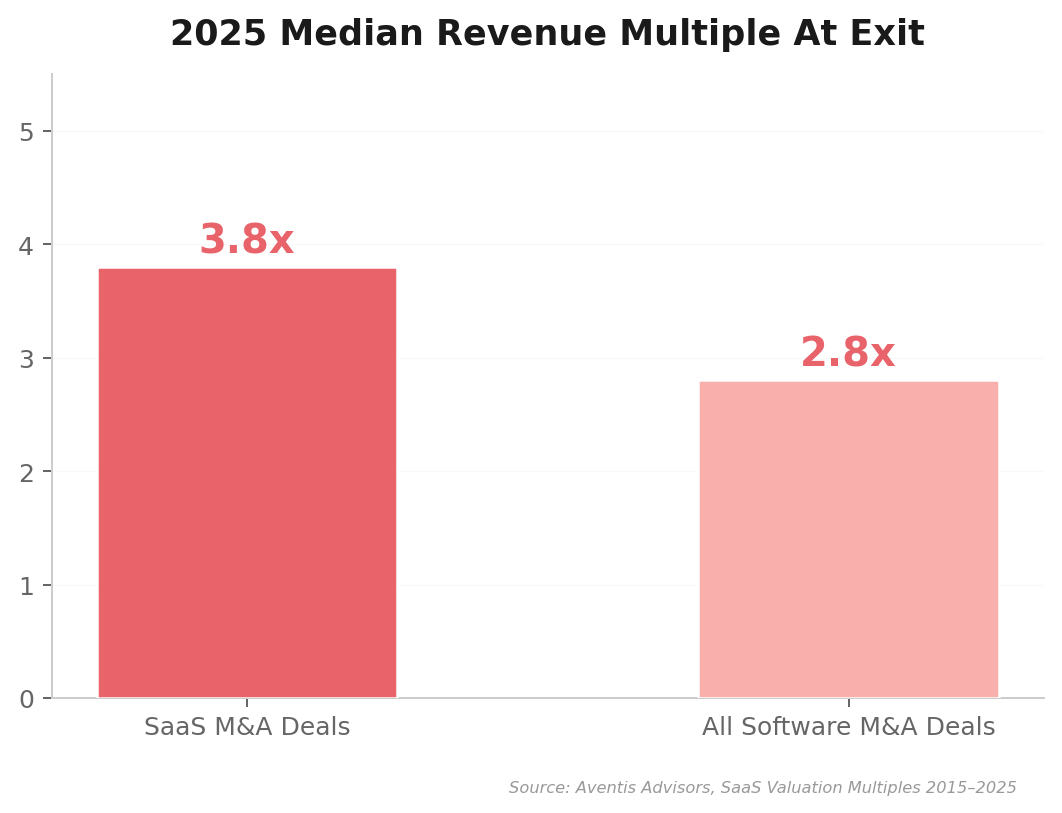

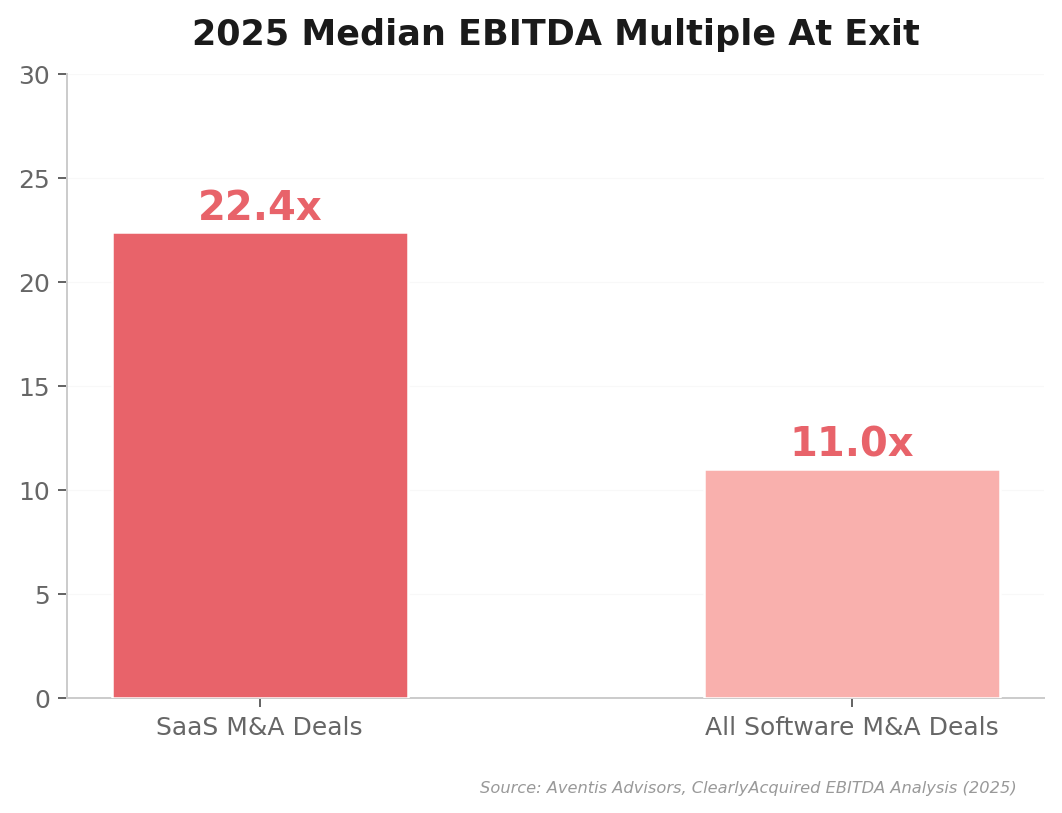

| M&A Exit (Private Transactions) | 3.8x | 8.1x+ | 🟡 Up from 2.9x in 2024 |

Key Insight: Private SaaS multiples have proven more resilient than public because private transactions rely on fundamental business metrics (ARR growth, NRR, profitability) rather than sentiment-driven market pricing. The public-to-private discount has actually narrowed, creating potential take-private opportunities for PE firms.

The Great Bifurcation

Perhaps the most important trend is the widening gap between winners and losers. The spread between top-quartile and bottom-quartile SaaS multiples has never been wider:

- Top quartile: AI-native, high-NRR, Rule of 40+ companies trading at 10x–15x+

- Median: Solid but traditional SaaS at 4x–6x

- Bottom quartile: Commodity horizontal SaaS facing AI substitution risk at 1x–3x

Windsor Drake's Q1 2026 report summarizes it well: "Founders face a binary outcome: achieve premium valuations through operational excellence (Rule of 40, AI integration, profitability) or face significant discounts as market bifurcation widens."

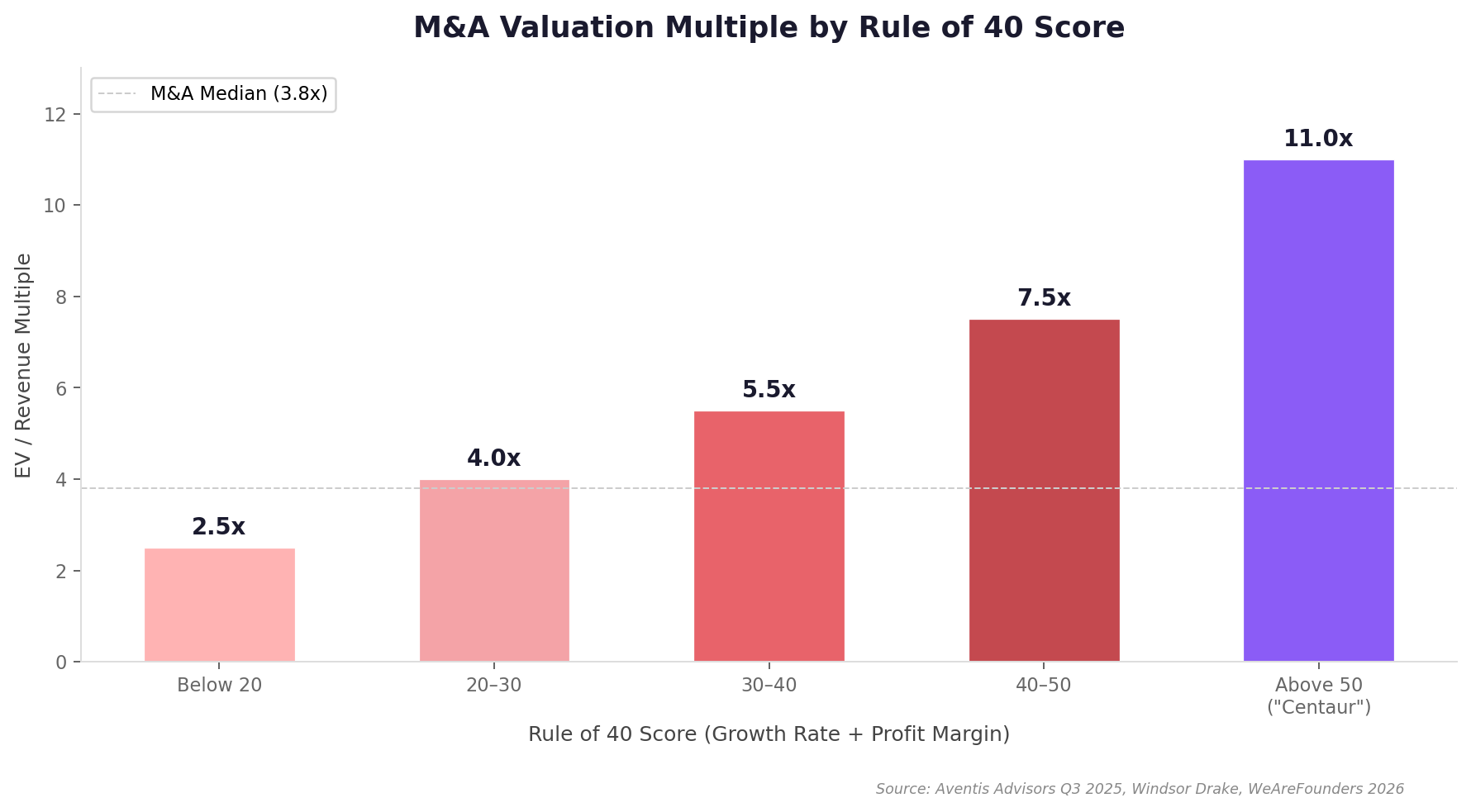

📐 The Rule of 40: The Defining Metric of This Era NEW

The Rule of 40 (Revenue Growth % + EBITDA Margin %) has emerged as the single most important metric for SaaS valuations. With growth rates slowing and AI compressing margins, the ability to demonstrate efficient growth has never been more valuable.

What the Data Shows

Aventis Advisors' analysis of 71+ public SaaS companies reveals:

- Each 10-point improvement in Rule of 40 corresponds to approximately a 1.1x–1.5x increase in EV/Revenue multiple.

- Companies above Rule of 40 attract premium valuations and stronger investor interest.

- Companies below Rule of 40 face lower multiples and tougher fundraising or exit negotiations.

- Companies above Rule of 50 ("Centaurs") can command double-digit multiples (10x+).

NRR: The Growth Quality Signal

Net Revenue Retention above 106% is the new growth lever. Companies with NRR above 106% grow 2.5x faster than those below that threshold. In a market where new customer acquisition costs rose 14% through 2025, expansion revenue from existing customers has become the primary growth engine.

The Formula for Premium Valuations in 2026:

Rule of 40 > 50 + NRR > 120% + Proprietary AI Integration = 7x–9x ARR

Add a competitive buyer process + $50M+ deal size = potential 10x–12x ARR (fewer than 5% of deals)

Revenue Multiples Showed Strength Early, Then Moderated

Public SaaS revenue multiples in 2025 initially showed strength, with the median reaching 6.1x by Q3 2025. However, the AI disruption fears that built through Q4 2025 and exploded in Q1 2026 have pushed the median back down to 5.1x–5.5x as of March 2026.

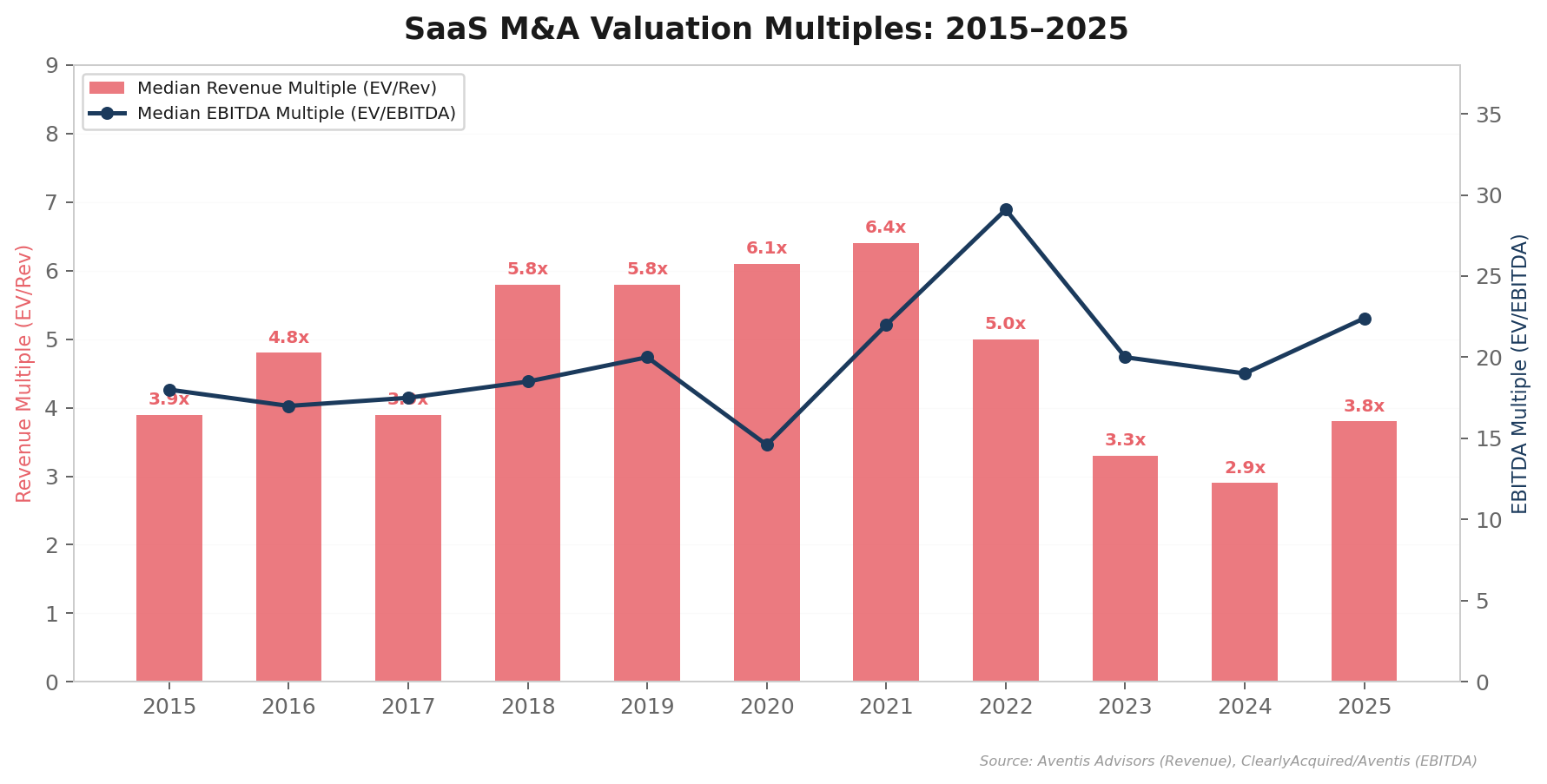

Revenue & EBITDA Multiples Over the Last 10+ Years

Between 2015 and 2025, the median SaaS company was valued at a median of 4.5x EV/Revenue. A quarter of companies achieved valuations above 8.1x. The pandemic peak of 2021 (18x+ median) now looks like a historic anomaly rather than a new normal.

The SaaS Valuation Premium Over Legacy Software Companies

Even after the SaaSpocalypse compression, SaaS companies retain a significant premium over traditional perpetual-license software. The recurring revenue model, higher gross margins, and better visibility into future cash flows continue to justify this premium—though the gap has narrowed.

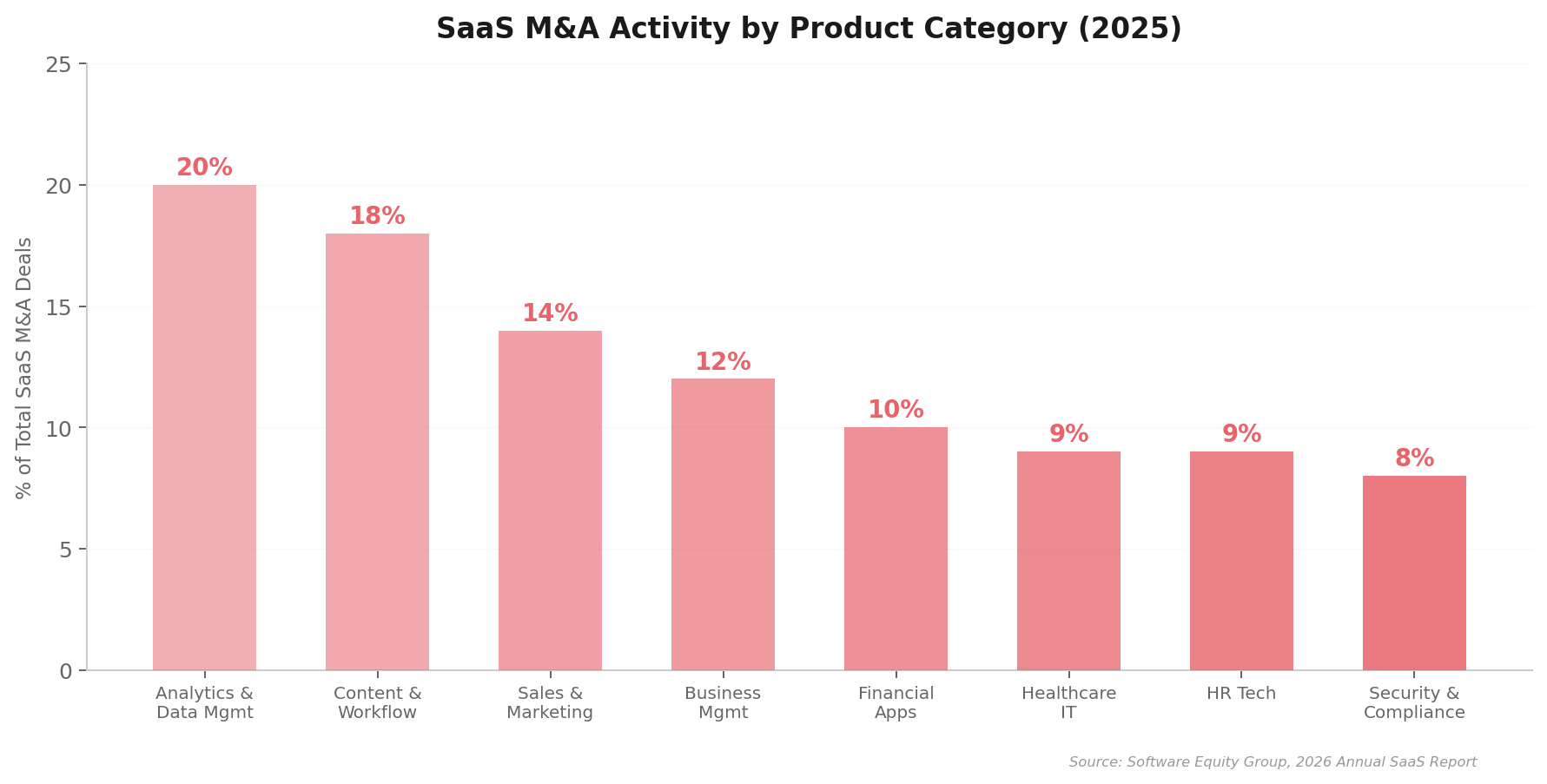

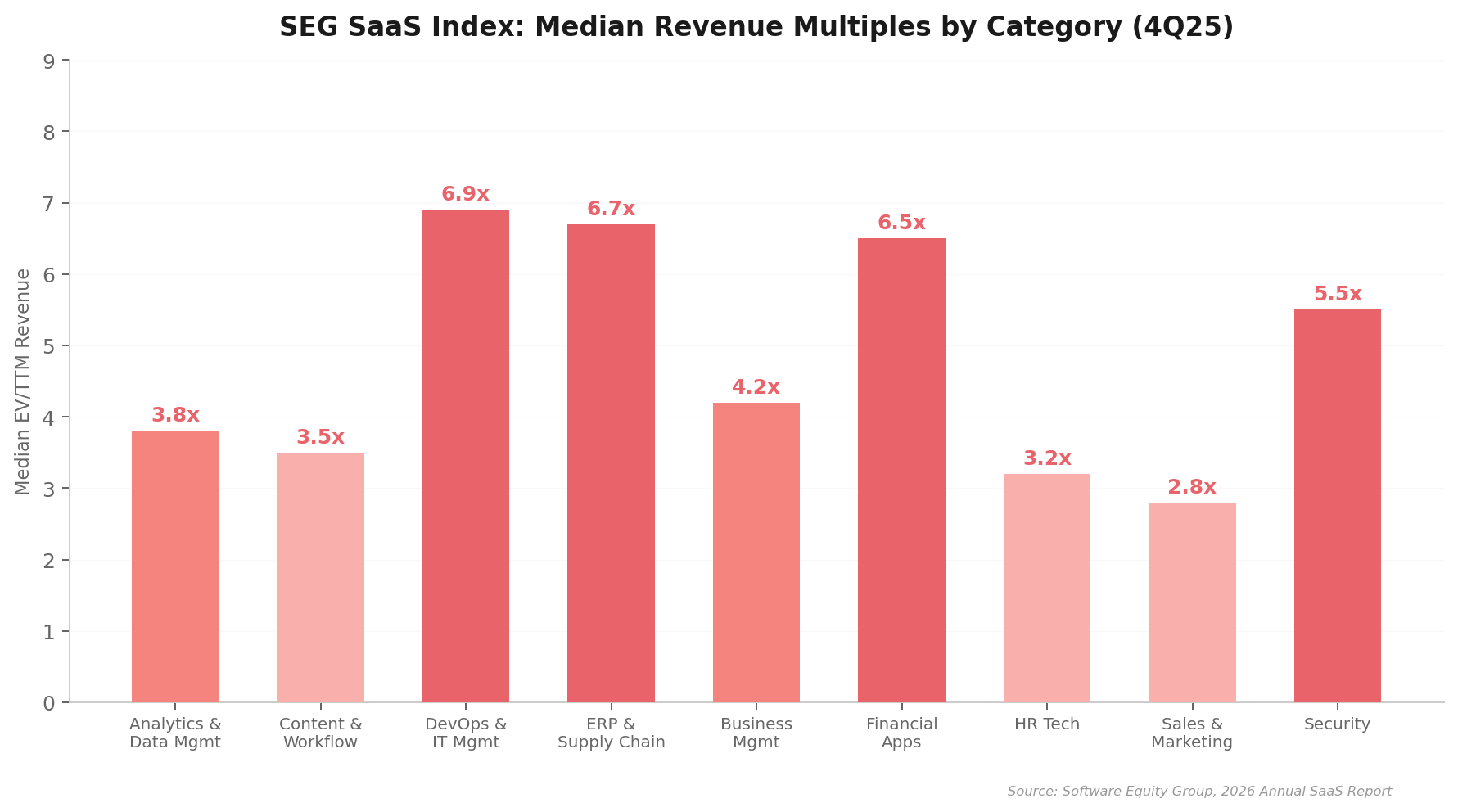

Revenue Multiples by SaaS Category

Vertical AI and cybersecurity command the highest multiples, while commodity horizontal tools face the steepest declines. The AI premium is real—but only for companies with proprietary models and embedded workflows, not thin AI wrappers.

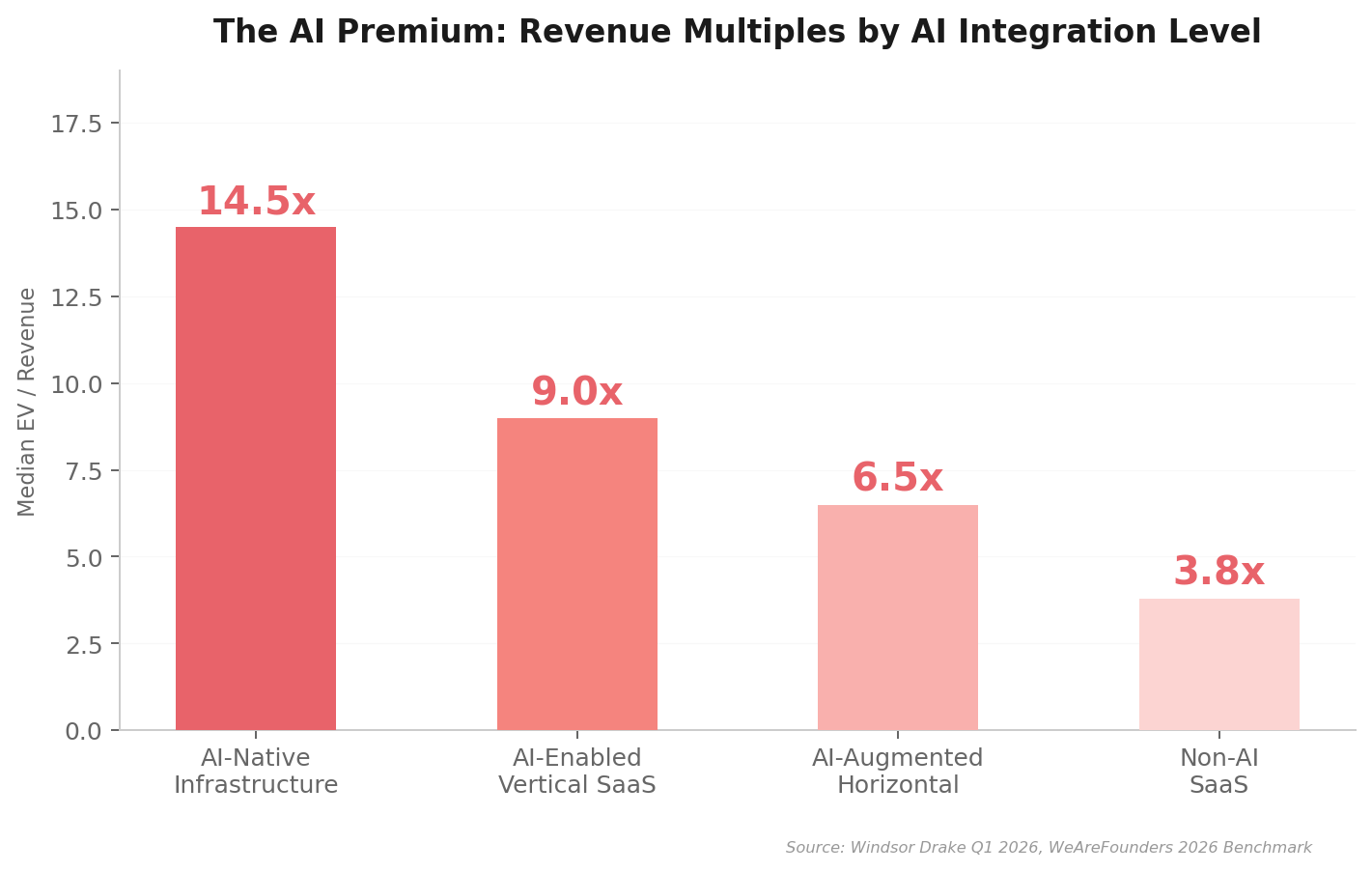

🤖 The AI Premium in SaaS M&A

AI-native companies are commanding 40–80% valuation premiums over comparable traditional SaaS in 2025–2026. But the market has become much more sophisticated about distinguishing real AI value from hype:

| AI Category | Median Multiple | Disruption Risk |

|---|---|---|

| 🟢 Vertical AI (proprietary models, deep industry) | 9.0x–12.0x | Low — moats from data & domain |

| 🟢 AI Infrastructure (compute, data streaming) | 8.0x–15.0x+ | Low — picks & shovels |

| 🟡 AI-Enhanced Incumbent SaaS | 5.0x–8.0x | Medium — depends on execution |

| 🔴 "AI Wrapper" (thin layer over LLMs) | 2.0x–4.0x | High — retention collapsing |

| 🔴 Commodity Horizontal SaaS (no AI) | 1.0x–3.0x | Critical — seat compression |

SaaS Categories Most Vulnerable to AI Disruption

| Category | Risk Level | Why |

|---|---|---|

| Customer Support Tools | 🔴 Critical | AI handles 80%+ of tier-1 tickets |

| Content Creation Platforms | 🔴 Critical | AI generates content at near-zero cost |

| Legal Research | 🔴 Critical | Claude Cowork's legal plugins |

| Data Analysis Dashboards | 🟠 High | AI agents query and analyze directly |

| Simple CRM Tools | 🟠 High | AI replaces data entry + basic automation |

| Developer Tools | 🟡 Medium | AI assists but doesn't replace IDE workflows |

| Enterprise ERP | 🟢 Lower | Deep integration + switching costs |

Hot M&A Sectors in SaaS

Four sectors dominated M&A activity in 2025:

- Cybersecurity ($70B+): Google/Wiz ($32B), Palo Alto/CyberArk ($25B), ServiceNow/Armis ($7.75B), Palo Alto/Chronosphere ($3.35B)

- AI Infrastructure & Tools ($30B+): Meta/Scale AI ($14.3B), CoreWeave/Core Scientific ($9.0B), OpenAI/io ($6.5B), OpenAI/Windsurf ($3B)

- Data & Analytics ($20B+): IBM/Confluent ($11B), Salesforce/Informatica ($8B), ServiceNow/Moveworks ($2.85B)

- Enterprise Software ($25B+): Thoma Bravo/Dayforce ($12.3B), Vista+Blackstone/Smartsheet ($8.4B)

Who's Buying: The Most Active Software Company Acquirers

| Acquirer | Major Deals in 2025 | Total Value | Strategy |

|---|---|---|---|

| Palo Alto Networks | CyberArk ($25B), Chronosphere ($3.35B) | $28.35B | Cybersecurity platform consolidation |

| Alphabet / Google | Wiz ($32B) | $32B | Cloud security moat |

| OpenAI | io Products ($6.5B), Windsurf ($3B) | $9.5B | AI hardware + dev tools |

| ServiceNow | Armis ($7.75B), Moveworks ($2.85B) | $10.6B | AI + cybersecurity expansion |

| IBM | Confluent ($11B) | $11B | Real-time data for AI |

| Salesforce | Informatica ($8B) | $8B | Data infrastructure for AI |

| Meta | Scale AI 49% stake ($14.3B) | $14.3B | AI data + talent acquisition |

The Top Software Investment Banks

The largest software M&A transactions in 2025 were advised by these leading banks:

| Bank | Notable Advisory Roles (2025) | Estimated Deal Volume |

|---|---|---|

| Goldman Sachs | Advised Hg on OneStream; multiple mega-deals | $60B+ |

| J.P. Morgan | Advised OneStream, HPE/Juniper | $50B+ |

| Morgan Stanley | Multiple cybersecurity & AI deals | $40B+ |

| Qatalyst Partners | Advised HPE on Juniper acquisition | $30B+ |

| Citigroup | Committed financing for HPE/Juniper | $25B+ |

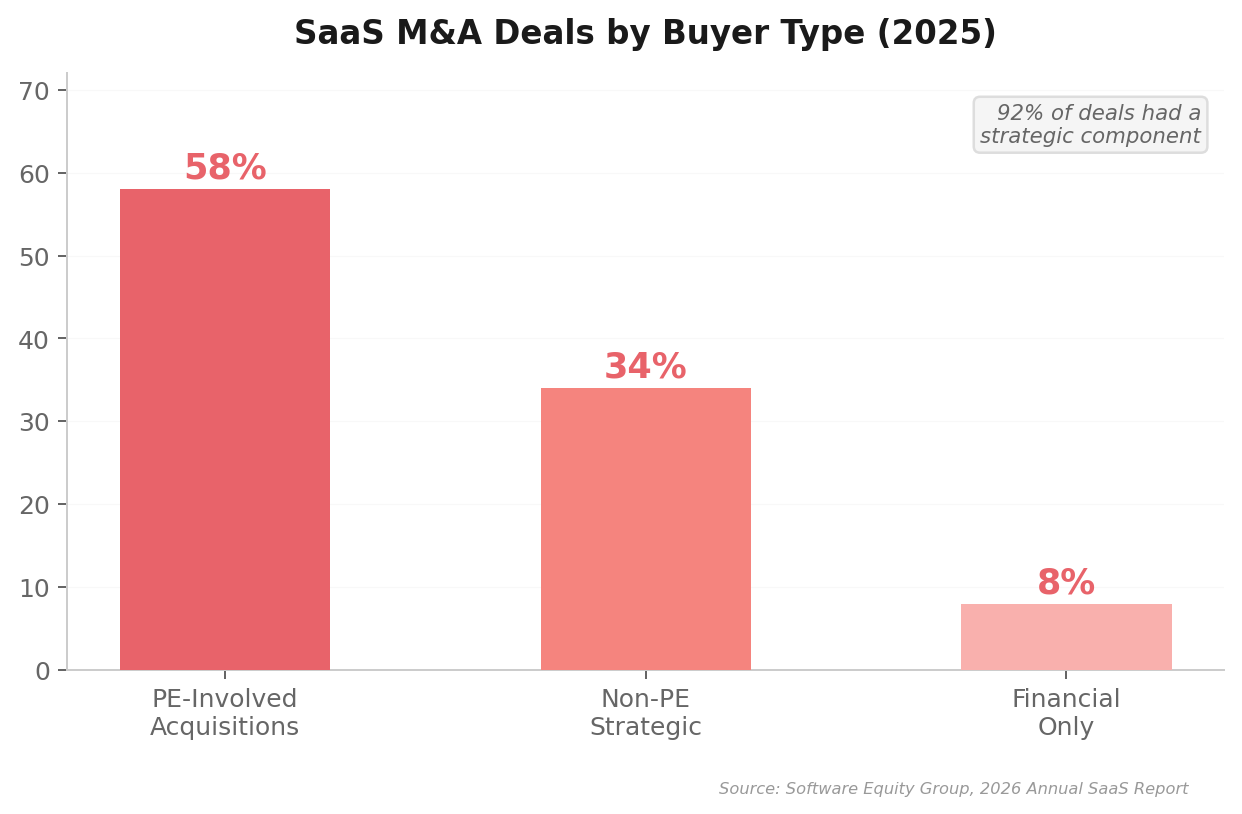

Types of Acquirer: Strategic vs. Private Equity

2025 saw a notable shift back toward strategic acquisitions, driven by the AI urgency. Companies like Google, Palo Alto, ServiceNow, and IBM were willing to pay premium multiples to acquire capabilities they couldn't build fast enough internally. PE buyers remained active (Thoma Bravo/Dayforce, Vista+Blackstone/Smartsheet, Hg/OneStream) but focused on take-private transactions of mature, profitable platforms.

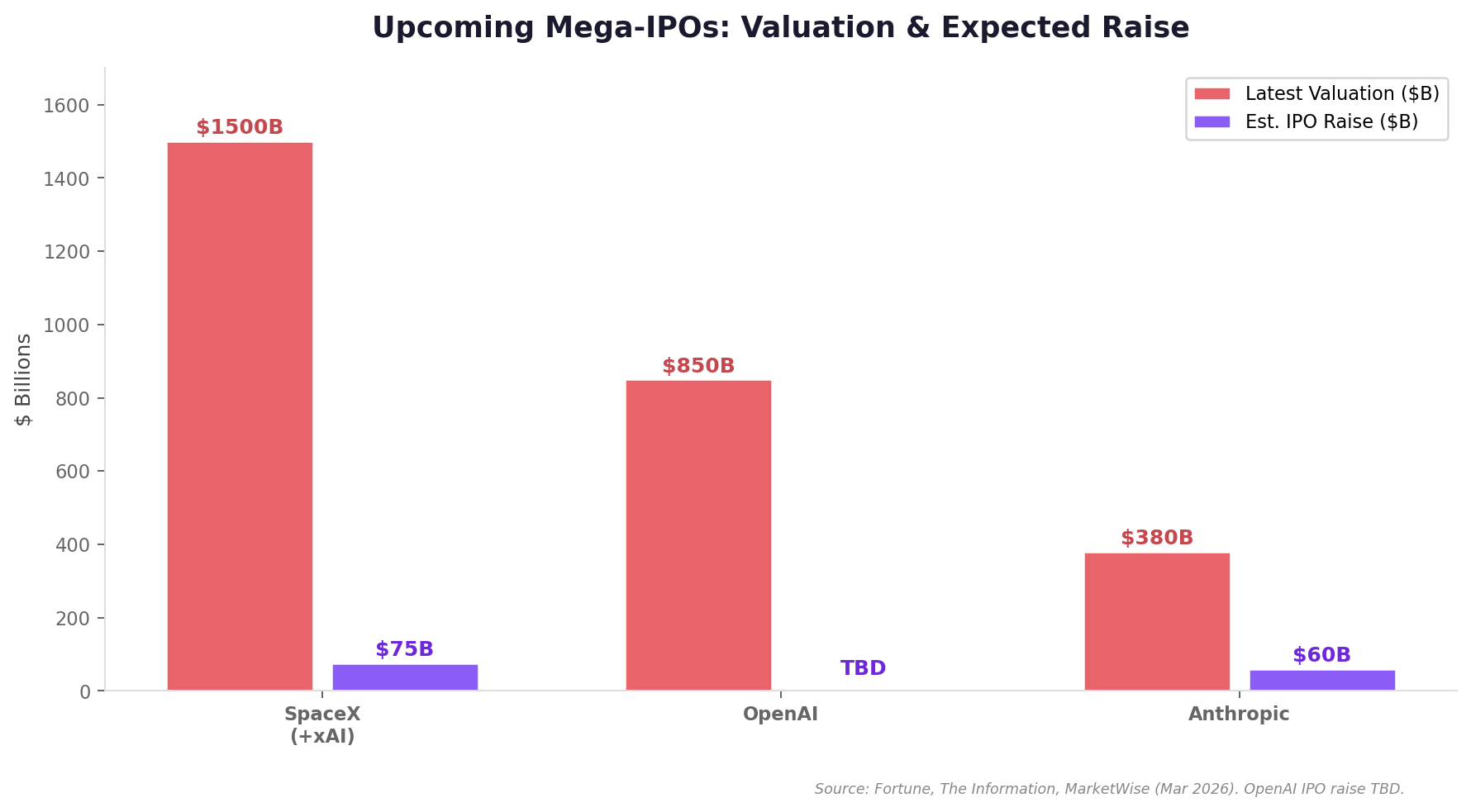

🚀 Upcoming Mega-IPOs: Anthropic, OpenAI & SpaceX NEW

Three upcoming IPOs have the potential to reshape public and private SaaS multiples for years to come. Their combined expected market caps exceed $2.5 trillion—larger than the entire public SaaS universe.

🟣 Anthropic — The SaaS Disruptor

| Metric | Detail |

|---|---|

| Latest Valuation | $380B (Feb 2026 round, $30B raised) |

| Revenue | $26B annualized (projected 2026) |

| Expected IPO Raise | $60B+ |

| Expected Timeline | Q4 2026 (per The Information, Mar 2026) |

| Key Backers | Alphabet, Amazon |

| Legal Counsel | Wilson Sonsini (IPO preparation) |

Anthropic's IPO would be transformative for SaaS because it's the company causing the SaaSpocalypse. If Anthropic's IPO succeeds at a $380B+ valuation while traditional SaaS stocks languish, it will definitively validate the thesis that value is migrating from the SaaS application layer to the AI model layer.

🟢 OpenAI — The AI Giant

| Metric | Detail |

|---|---|

| Latest Valuation | $852B (Apr 1, 2026; $122B raised — largest private fundraise in history) |

| Revenue | $24B+ annualized ($2B/month as of Apr 2026); growing 4x faster than Alphabet/Meta at same stage; targeting $100B by 2027 |

| Annual Losses | ~$40–50B/year (per Microsoft 27% stake write-down) |

| Corporate Structure | Restructured to for-profit PBC (Nov 2025) |

| Expected Timeline | Late 2026–2027 |

| Key Investor | Co-leads: SoftBank, a16z, D.E. Shaw, MGX, TPG, T. Rowe Price. Also: Amazon, Nvidia, Microsoft (~$3B retail). Microsoft retains 27% ownership |

OpenAI’s $122B raise on April 1, 2026—the largest private fundraise in history—valued the company at $852B post-money. Business revenue now accounts for 40% of total revenue (up from ~30%), with consumer-enterprise parity expected by year-end 2026. Despite $40–50B in annual losses, the restructuring to for-profit PBC and the sheer scale of its revenue growth make an IPO “inevitable” per multiple analysts.

🔵 SpaceX (+xAI) — The Mega-IPO

| Metric | Detail |

|---|---|

| Latest Valuation | $1.25–1.5T (post xAI merger, Feb 2026) |

| Expected IPO Raise | $50–75B |

| Expected Timeline | Mid-2026 (June) |

| Key Assets | Falcon 9, Starship, Starlink, xAI (Grok) |

| Significance | Would be 2nd largest IPO in history (after Saudi Aramco) |

SpaceX's IPO would be the largest tech IPO ever. At $1.5T, it would instantly become one of the 10 most valuable companies on Earth. While not a traditional SaaS company, the xAI integration (Grok) and Starlink's recurring revenue model make it highly relevant to SaaS investors. PitchBook's Franco Granda believes $1.75T is justifiable based on Starlink's growth trajectory.

Impact on SaaS Multiples

These IPOs will have a complex effect on SaaS valuations:

- Positive: Success validates AI/tech at massive scale, potentially lifting all boats through renewed investor enthusiasm

- Negative: These IPOs could absorb significant capital from institutional investors, reducing allocations to existing SaaS holdings

- Structural: They reinforce the thesis that value is migrating to AI model providers and infrastructure, away from traditional SaaS application layer

The Outlook for SaaS M&A in 2026

Despite—or perhaps because of—the SaaSpocalypse, we expect 2026 to be another strong year for SaaS M&A:

- PE Take-Privates Will Accelerate: With public SaaS stocks trading at depressed multiples, PE firms with record dry powder will exploit the discount. Expect more Dayforce/Smartsheet-style take-private deals.

- AI Consolidation Wave: Strategic acquirers will continue buying AI capabilities. OpenAI's acquisitions of Windsurf and io Products signal the AI leaders are building full-stack platforms through M&A.

- Cybersecurity Remains Hot: Palo Alto's $28B+ in deals shows the sector's appetite. As AI creates new attack vectors, security spending will remain resilient.

- Distressed SaaS Opportunities: Companies most exposed to AI substitution (customer support, content creation, simple CRM) may become acquisition targets at discounted multiples.

- The IPO Window May Reopen: If Anthropic, OpenAI, and SpaceX IPOs succeed, they could reignite appetite for tech IPOs more broadly.

Our 2026 Predictions:

- Public SaaS median multiples stabilize at 5.0x–6.0x

- Private SaaS median venture deal multiples stabilize at 4.2x–5.2x

- Private SaaS M&A multiples stabilize at 3.8x–4.8x

- AI-native premium multiples expand to 10x–18x for best-in-class

- M&A deal volume reaches $200B+ as PE take-privates accelerate

- At least 3 more mega-deals (>$10B) will be announced

- The IPO market reopens with 5+ SaaS/AI IPOs in H2 2026

The Five Big Questions to Ask Before Selling Your Software Firm

- Is your Rule of 40 above 40? If not, focus on getting there before going to market. The premium is real and measurable: each 10-point improvement = ~1.5x higher multiple.

- Is your NRR above 106%? Companies with NRR above 106% grow 2.5x faster and attract significantly higher multiples. If your NRR is below 100%, fix churn before pursuing an exit.

- Do you have a defensible AI story? In 2026, acquirers want to know: How does AI help your product? How does it threaten it? Can you articulate a credible AI roadmap?

- Is your ARR growing 30%+ YoY? Growth rate remains the single most weighted variable in valuation formulas. Below 15%, expect low single-digit multiples.

- Can you run a competitive process? The median is 4–6x, but competitive processes with multiple bidders consistently achieve 7–10x+. Running a proper dual-track (M&A + IPO) or multi-bidder process is essential for premium outcomes.

Tips to Prepare Your Software Firm For An Exit

- Get your metrics pristine: Buyers will scrutinize ARR, NRR, gross margin, Rule of 40, and LTV/CAC. Have these auditable and defensible.

- Build an AI narrative: Even if AI isn't your core product, show how you're integrating it and how it strengthens (not threatens) your business.

- Focus on profitability: The era of "growth at all costs" is over. Demonstrate a clear 24-month path to EBITDA positive.

- Invest in customer success: NRR above 120% can nearly double your multiple. Expansion revenue is the most efficient growth engine in this market.

- Hire an experienced banker: The top banks (Goldman Sachs, JP Morgan, Qatalyst) justify their fees many times over through competitive process management and buyer relationships.

- Time the cycle: With PE dry powder at records and interest rates favorable, the M&A window is open. Don't wait for conditions that may not improve.

Conclusion

The SaaS industry is undergoing its most significant transformation since the advent of cloud computing. The SaaSpocalypse has exposed the vulnerability of seat-based pricing models to AI disruption, while simultaneously creating opportunities for founders who can adapt.

The data is clear: 2025 was a record year for SaaS M&A, and 2026 is shaping up to be even bigger. But the rules have changed. Premium valuations now require a combination of efficient growth (Rule of 40+), strong retention (NRR 105%+), and a credible AI integration strategy.

For founders considering an exit, the window is favorable. Record PE dry powder, lower interest rates, and strategic urgency around AI are creating competitive M&A processes. For those building, the message is equally clear: AI isn't optional. Companies that embrace AI transformation will thrive; those that don't will see their multiples—and their relevance—continue to compress.

The SaaSpocalypse isn't the end of SaaS. It's the beginning of a new chapter where the winners are defined by AI capability, operational efficiency, and the ability to deliver measurable outcomes—not just seats.

Want to connect with other SaaS CEOs navigating this landscape?

Join 400+ SaaS founders at SaasRise — the premier mastermind community for B2B SaaS CEOs scaling from $1M to $100M+ ARR.

Learn More at SaasRise.com →Sources & Methodology

This report draws on data from the following sources, all accessed and verified in March–April 2026:

- SaaS Capital Index (SCI) — Monthly B2B SaaS valuation benchmark

- Aventis Advisors — SaaS Valuation Multiples 2015–2025 reports

- Windsor Drake — SaaS Valuation Report Q1 2026

- Cooley LLP — 2025 Tech M&A Year in Review

- Bain & Company — "Why SaaS Stocks Have Dropped" (Feb 9, 2026)

- NxCode — "SaaSpocalypse 2026" analysis (Feb 5, 2026)

- Softwareseni — "The SaaS Reckoning Explained" (Mar 23, 2026)

- Financial Content / MarketMinute — "The SaaSpocalypse of 2026" (Mar 30, 2026)

- Menlo Ventures — Enterprise AI Spending Report (2025)

- WeAreFounders — 2026 US SaaS Valuation Multiples Benchmark

- The VC Corner — "What's Your SaaS Company Worth in 2026?" (Mar 18, 2026)

- Investing.com, Built In / Fortune, MarketWise, EBC — IPO analysis reports

- The Information — Anthropic IPO timeline (Mar 26, 2026)

- Company press releases from: Google, Palo Alto Networks, IBM, ServiceNow, CoreWeave, AMD, Salesforce, OpenAI, HPE, Hg Capital, Capital One

- S&P Capital IQ, PitchBook, Dealroom — Deal data and market analytics

Rise Worldwide, Inc. | 3609 Country White Lane, Austin, TX 78749